- Securitization in its simple form (plain vanilla) contributes to sustainable growth by increasing the supply of credit in the economy and thus bringing down its cost.

- Israel has an incentive to develop the securitization market since it can provide a bridge between sources (funds in the hands of institutional investors) and uses (the sectors and enterprises that are in need of credit, including small and medium-sized businesses, infrastructure projects and rental housing projects).

- The encouragement of securitization can reduce funding costs and expand the variety of investment channels available to institutional investors and the public.

- Securitization can help the banking system free up capital in order to provide new loans, including loans to small and medium-sized businesses. This is because the Banking Supervision Department will permit the securitization of a variety of credit loans, including loans to small and medium-sized businesses (SMEs).

- The attempt to promote securitization seeks to create a balance between the advantages of development of the securitization market in a gradual and balanced manner and the risks inherent in financial development, by paying heed to the lessons learned from the global financial crisis, among other means.

- The measures proposed in the Interim Report for Promoting Securitization are meant to reduce the moral hazard implicit in the instrument and will facilitate the correct valuation of risk in the securitization market.

Background

Securitization is common in advanced economies because it is a tool that expands the sources of financing for the business sector, increases competition and supports the dispersion of risk among the various players in the capital market.

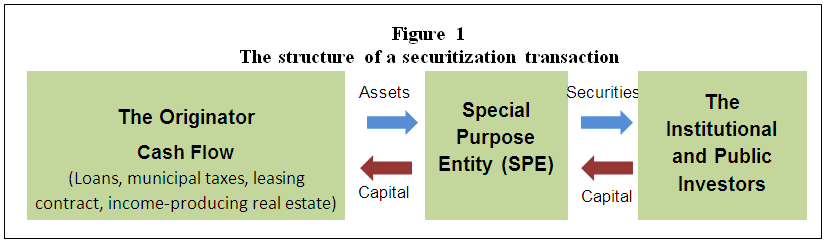

As shown in Figure 1, banks or other types of originators in a securitization transaction sell the rights to assets that produce a cash flow to a special purpose entity (SPE), and the SPE issues securities to the investing public and transfers the proceeds to the originator. The SPE serves therefore as a conduit through which the cash flow from the assets flows until the security matures. To illustrate, if an originator holds a real asset, such as a rental housing project, and wishes to finance a new project, the rights in the existing project can be sold to the SPE and the SPE will issue securities to investors and service them using the rental payments. Similarly, if an originator holds a financial asset, such as a bank that provides loans to small businesses and wishes to free up credit sources in order to provide new loans, it can sell its rights in the existing loans to an SPE and the SPE will issue securities and pay investors using the cash flow from the loans.

The originator has an incentive to carry out securitization since the transaction provides him with a capitalized and liquid amount of cash in the present in exchange for the sale of a future cash flow. The originator thus frees up capital to provide new credit or for real activity. The incentive for investors is that they receive an asset-backed security and are not exposed to the risk of the originator defaulting. A wide variety of underlying assets can be securitized: credit to small and medium-sized businesses, debts of credit card holders, mortgages, municipal taxes, leasing contracts, rent, etc.

Israel has an incentive to open up a securitization market since it can serve as a bridge between sources and uses, i.e., between funds in the hands of institutional investors (the quantity of which is growing at an increasing rate as a result of the reforms carried out in pension savings) and sectors and enterprises that are in need of credit, including small and medium-sized businesses, infrastructure development, rental housing projects, etc. The banking system and real companies with stable cash flows can use securitization in order to raise capital to fund their activity.

Securitization in its simple form contributes to sustainable growth since it increases the supply of credit in the economy and thus lowers its cost. Research indicates that financial development supports real economic development[1] and securitization has become one of the pillars of a developed capital market. However, alongside its advantages, securitization also suffers from a disadvantage since in the absence of appropriate regulation it may have an adverse effect on the stability of the financial market. Evidence of this is the crisis that developed in 2008 in the US.

This situation is what guided the work of the Joint Team to Promote Securitization in Israel. In order to encourage securitization, while at the same time maintaining the stability of the financial system, the team formulated guidelines intended to create transparency regarding the underlying assets and prevent over-complexity in their securitization, to isolate the risk to securitized assets only, to separate between the originator and the SPE and to strengthen the alignment of interests between the originator and investors. These guidelines, along with ongoing and stringent supervision, will make it possible to develop the securitization market in a gradual and balanced manner and to maintain financial stability. The team published a report for the public’s comments in August 2014.[2]

The scope of securitization worldwide increased rapidly in the early years of the previous decade; however, it declined considerably following the financial crisis. During 2009, the market began to recover, primarily because central banks supported it based on the belief that securitization is an important tool that can be used to strengthen the financial system and as a means of encouraging the real economy.

Despite the problems revealed by the crisis, there is a consensus that the securitization market will continue to be an important component of the international financing market. A report issued by the Bank of England and the European Central Bank, for example, states that “The [securitization] market is shrinking. This is a concern because securitization, if appropriately structured and regulated, can complement other long-term wholesale funding sources for the real economy, including for small and medium-sized enterprises (SMEs).”[3] This approach rests on the fact that in securitization markets with robust foundations, failures have not occurred and the market has continued to function. Thus, the cumulative default rate on European consumer-related securitization was only 0.05 percent from July 2007 until the third quarter of 2013.[4] Furthermore, the problem in the US securitization market is concentrated on the securitization of high-risk (sub-prime) mortgages.[5]

Effects of the securitization market on the financial system

a. The advantages of the securitization market

The reduction in the cost of sources of financing and their expansion: Securitization isolates the risk to investors to that of the securitized assets only. In other words, it does not expose them to the default risk of the originator, and the isolation of risk can be expected to raise the credit rating. Securitization will therefore make things easier for both investors and originators. Investors will be able to better evaluate the risk involved and the originators will be able to raise capital at lower interest rates, particularly if they do not have a high credit rating and they are securitizing high-quality assets. Medium-sized and large firms will be able to directly obtain credit by means of securitization and in this way to focus on their real activity rather than their financial activity.

Expansion of investment channels and development of a non-bank credit market: Institutional investors and the public will be exposed to a variety of assets that produce a predetermined cash flow. The securitization of assets will therefore offer a new investment channel, backed up by high-quality collateral, for the public’s long-term savings. This channel became particularly relevant following the structural reforms carried out in the economy, which increased long-term savings and led to a continuous increase in the amounts of money managed by institutional investors. This alternative will compete with investment in corporate bonds, a channel that in certain periods raises the concern of overvaluation due to the small number of investment alternatives. Reduced concentration in the supply of credit will increase competition and will make it easier to obtain funding for real activity in the economy.

Freeing up of capital in the banking system: The banking system is limited in its ability to provide new credit, but it has an advantage in the underwriting of loans and in their ongoing management. Although, as noted, the amount of savings is growing, institutional investors do not have expertise in underwriting and providing credit to many types of borrowers. Securitization will enable the banking system to shift part of its liabilities and its risk to the capital market and thus free up sources of funds that can be used to provide new loans to the sectors that are in need of credit, while at the same time improving the accessibility of the sources for a variety of businesses. Since bank credit is used by small and medium-sized businesses in Israel as the almost exclusive source of external financing, securitization is critical in order to ease the financial constraints on them.

It is the intention of the Banking Supervision Department to permit securitization of a variety of types of credit, including loans to small and medium-sized businesses (SMEs), with the goal of increasing the supply of credit to this sector. Nonetheless, it is also the intention of Bank Supervision to leave in place the regulations prohibiting complex transactions (such as CDOs and CDO2s), as recommended in the report published by the team to promote securitization. This is meant to prevent the issue of complex instruments and to facilitate more accurate valuation of the risks implicit in the underlying assets.

As can be seen in Figure 2, the securitization of loans to small and medium-sized businesses (SMEs) in Europe accounts for a significant and growing share of securitization transactions. Some countries require banks to provide new credit to small businesses in exchange for government support in securitization.

a. Maintaining the stability of the financial system

The securitization market can, as noted, increase competition in the capital market and the supply of credit, but there are risks implicit in securitization that need to be addressed. Every investment involves risk and like every other investment a balance must be found between the risk and reward.

Moral hazard: Moral hazard exists when the originator creates assets that will be sold in the future by means of securitization and does not bear the consequences of the risk implicit in the assets. This situation incentivizes the originator to ex ante (i.e., before the securitization is carried out) create risks that are greater than the expected profit and to transfer them onward to other players in the capital market chain and exploit the capital received in order to create new assets to sell (a strategy known as “generate to distribute”). Thus, a flawed structure of incentives is created, since it encourages the creation of low-quality assets which are intended for sale.

An initial response to this risk involves the ongoing regulation of the institutions that manage the public’s funds, as in the case of the existing regulation of investment in other assets. A second response involves strengthening the alignment of interests between the originator and the investors by means of regulation that requires the originator to retain part of the risk. In that case, if a credit failure occurs, the originator will experience a loss as well. The more risk that is left with the originator the greater the alignment of interests between the originator and the investors in the SPE. However, since the securitization process involves a fixed cost, if too high a proportion of the asset is left with the originator then the size of the securitization transaction will be reduced to the point where it will not be worthwhile. This is the reason that prior to the financial crisis and until recently there was no obligation to retain any part of the risk with the originator, even in the case of high-risk loans, and therefore alignment of interests between the originator and the investors was not achieved, even in part.[6]

A third response to the problem of moral hazard relates to repeat players and the risk to reputation. Credit failure in a large number of securitized assets will harm the reputation of the originator. This will make it difficult for that entity to raise capital in the future, and also involves a not-insignificant economic price. Regulations that ensure a true sale and prohibit the support of liquidity—regulations which were not in place around the world prior to the crisis—will make it possible to, among other things, incentivize repeating players in the securitization market to ensure the quality of the assets they securitize.

Valuation of the assets: There is a structural information gap between the originator and the investors with regard to the value of securitized assets. The originator has no incentive to reveal information that is likely to lower the valuation of the asset, a phenomenon known as adverse selection, and in the long run a non-transparent market may lead to a prolonged deterioration in the quality of assets (“market for lemons”).[7]

The main solution to this problem involves demanding greater transparency with regard to the securitized assets. Transparency will reduce the information gap between the originator on one hand and the investors and credit rating agencies on the other, and will help achieve more accurate valuations. To this end, the Team to Promote Securitization proposed a supplementary measure: to prohibit complex securitization (CDOs and CDO2s) in order to provide a solution to cases in which the securitized assets are too complex for analysis and valuation. These supplementary measures will reduce the risk of flawed valuation and make securitization a more preferable instrument than corporate bonds from the point of view of valuation.

The ratings agencies have a critical role in the valuation of assets in securitization, since investors generally rely on their ratings. In view of the failure of the ratings agencies prior to the global crisis, they have revised their methodologies for evaluating the risk of structured financial instruments.[8] In addition, they are now subject to new regulations, both in Israel and worldwide. The new regulations have formalized their activity and require them to operate in a more cautious and responsible manner.[9]

The securitization market in Israel

While in a number of countries the securitization market has grown to a size similar to that of the corporate bond market, in Israel the market is almost non-existent. According to a ranking by the World Economic Forum in 2012, Israel’s securitization market was 54th in size out of 59 countries. The few securitization transactions carried out in Israel have been concentrated in leasing and income-producing realty, and they are carried out based on a specific legal opinion and without a comprehensive framework. Starting in the 1990s, several government committees recommended the development of the securitization market in Israel. The obstacles preventing that development involve legislation, taxation, regulation and accounting issues. The report produced by the Team to Promote Securitization includes detailed proposals for amending legislation that are meant to remove these obstacles. The report lays the foundation for the securitization of a variety of assets, such as credit to small and medium-sized businesses, retail loans and income-producing real estate, in the belief that this instrument can inject capital into the real economy. The recommendations in the interim report produce a balance between the inherent risk in financial development and the rewards of the gradual and cautious development of this important market.

[1] There is a vast literature on this topic. See, for example:

Greenwood, J. and B. Smith (1997), "Financial Markets in Development and the Development of Financial Markets", Journal of Economic Dynamics and Control 21(1), pp.145-81. Levine, R. (1997), "Financial Development and Economic Growth: Views and Agenda", Journal of Economic Literature 32(2); Levine, R. and S. Zervos (1998), "Stock Markets, Banks, and Economic Growth", American Economic Review, June, pp. 537-558.

[2] The team included representatives of the Israel Securities Authority, the Ministry of Justice, the Capital Market, Insurance and Savings Department at the Ministry of Finance, the Tax Authority, and the Bank of Israel, which coordinated the team’s work. An interim report issued by the team can be found at: http//:www.boi.org.il/he/NewsAndPublications/PressReleases/Pages-12-08-2014/Securitization.aspx

[3] See: European Central Bank and Bank of England (2014), "The Impaired EU Securitisation Market: Causes, Roadblocks and How to Deal With Them".

[4] The rate of default on asset-backed securities (ABS), residential mortgage-backed securities (RMBS) and collateralized loan obligations of small and medium-sized enterprises (SME CLO) stood at 0.04 percent, 0.1 percent and 0.4 percent respectively. Details appear in the discussion paper published by the Bank of England:

Bank of England (2014), "The Case for a Better Functioning Securitization Market in the European Union", A Discussion Paper.

[5] The rate of default on asset-backed securitization was only 0.36 percent in 2012 and only 0.61 percent in 2010.

Standard & Poor's (2013), Global Structured Finance Default Study, 1978-2012: A Defining Moment For Credit Performance Stability.

[6] The regulations in the US and Europe have adopted a rate of 5 percent of risk to be left with the originator. However, with respect to qualified mortgages in the US the rate is actually zero. In contrast, the Team for Promoting Securitization in Israel recommended a rate of 10 percent.

[7] Akerlof, G.A. (1970) "The Market for ‘Lemons': Quality Uncertainty and the Market Mechanism”, The Quarterly Journal of Economics, Vol. 84, No. 3.

Much has been written about what led the US into the sub-prime crisis, including the inaccurate estimation of risk. See, for example: Gorton, G.B. (2008), "The Panic of 2007", NBER WP/14358; Gorton, G.B. (2008), "The Subprime Panic", NBER WP/14398

[8] The Israeli branches of the international rating companies use the international methodology.

[9] Law for Regulating the Activity of Credit Rating Agencies – 2014 and the regulations based on it will go into effect in April 2015.