This document presents the forecast of macroeconomic developments compiled by the Bank of Israel Research Department in July 2018[1] in terms of the main macroeconomic variables—GDP, inflation and the interest rate. According to the staff forecast, gross domestic product (GDP) is projected to increase by 3.7 percent in 2018, compared with 3.4 percent in the previous forecast, and by 3.5 percent in 2019, similar to the previous forecast. The rate of inflation over the next year (ending in the second quarter of 2019) is expected to be 1.4 percent, compared with 1.2 percent in the previous forecast. The Bank of Israel interest rate is expected to increase to 0.25 percent in the fourth quarter of the year, and to increase once more in the third quarter of 2019.

Forecast

The Bank of Israel Research Department compiles a staff forecast of macroeconomic developments on a quarterly basis. The staff forecast is based on several models, various data sources, and assessments based on economists’ judgment.[2] The Bank’s DSGE (Dynamic Stochastic General Equilibrium) model developed in the Research Department—a structural model based on microeconomic foundations—plays a primary role in formulating the macroeconomic forecast.[3] The model provides a framework for analyzing the forces that have an effect on the economy, and allows information from various sources to be combined into a macroeconomic forecast of real and nominal variables, with an internally consistent “economic story”.

a. The global environment

Our assessments of expected developments in the global economy are based mainly on projections by international institutions (the International Monetary Fund and the OECD) and by foreign investment houses. These institutions revised their forecasts for growth and inflation in advanced economies and for world trade only slightly since their previous forecasts. Accordingly, our assessments are that growth in the advanced economies will be about 2.4 percent in 2018 and 2.1 percent 2019, and that imports to the advanced economies will increase by 5.0 percent in 2018 and by 4.7 percent in 2019. According to the assessments of investment houses, the US federal funds rate is expected to be 2.4 percent at the end of 2018 and 3.0 percent at the end of 2019. The declared interest rate in the eurozone is expected to be 0.0 percent at the end of 2018, and 0.2 percent at the end of 2019.

Additionally, our assessment is that inflation in the advanced economies will reach about 2.1 percent in 2018 and 2.0 percent in 2019. The price of Brent crude oil increased from an average of about $67 per barrel in the first quarter of 2018 to an average of about $75 per barrel in the second quarter.

b. Real activity in Israel

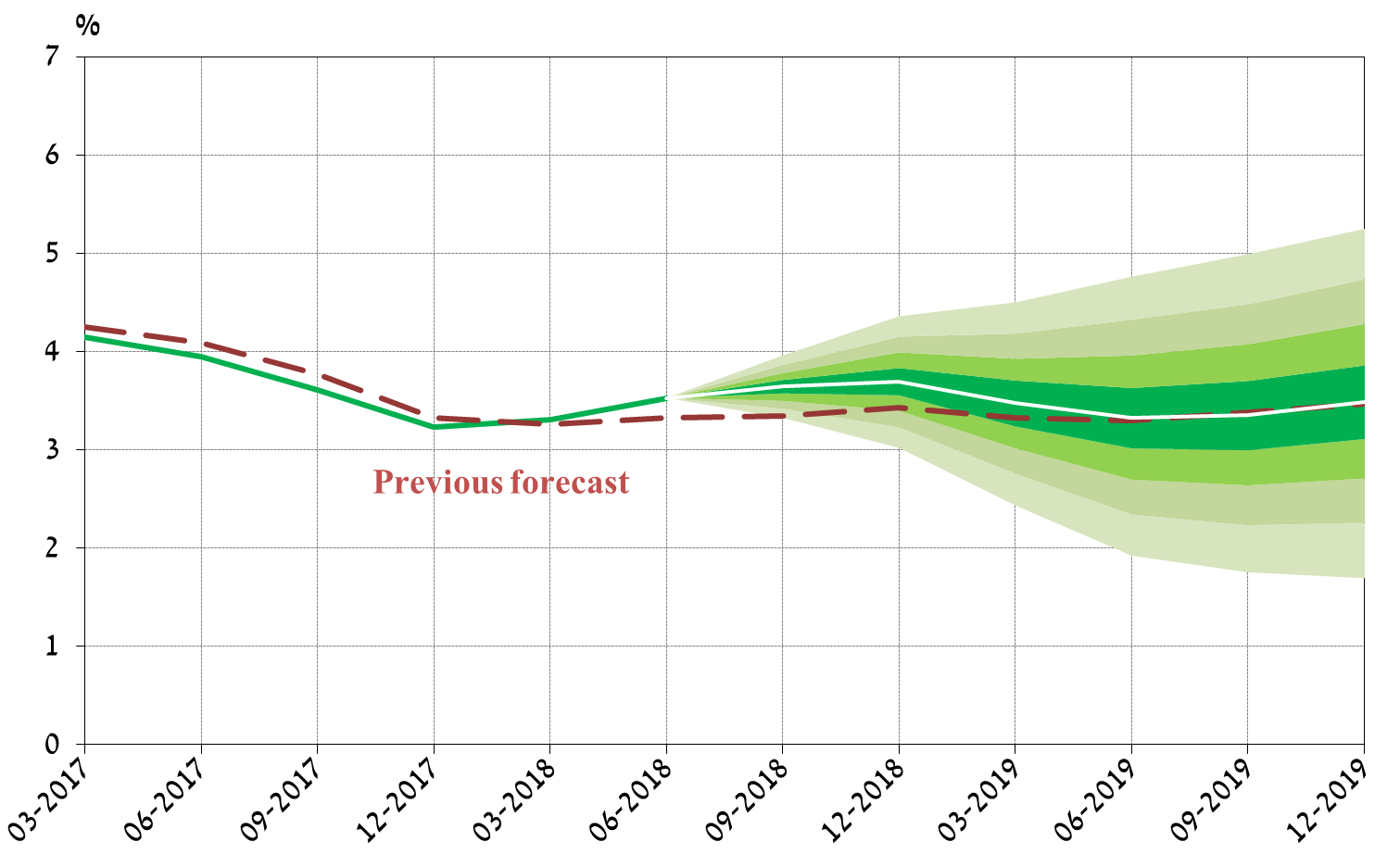

GDP is expected to grow by 3.7 percent in 2018 and by 3.5 percent in 2019 (Table 1). The expected growth rate for 2018 was increased, but there is no change in our basic assessments of forecast real developments in 2018 and 2019 relative to the previous forecast. The changes in the forecast of real developments are due to the base effect of the revision of Central Bureau of Statistics data for 2017 and the beginning of 2018, which contributed to an increase in the forecast of economic activity in 2018; the delay of the update of green taxation on vehicles, which contributed to lowering the forecast of real activity in 2018 and to an increase in the forecast of real activity in 2019; and revisions in the number of large investments (import-oriented) in the economy and regarding a continued slowdown in building starts in 2018.

Exports are expected to continue increasing at a high rate relative to previous years, inter alia because the assessments in the forecasts for world trade are that growth will continue at a relatively high rate, and in view of the maturation of a number of investments in various industries. Imports are expected to continue increasing at a rate higher than the GDP growth rate, while the labor market remains tight and the economy is around the GDP potential, exports are increasing, and import and customs barriers are lowered. The slowdown in investment in residential construction, which is reflected in the relatively low level of buildings starts in 2017 and the beginning of 2018, is contributing to a decline in the expected growth rate of fixed capital formation.

|

Table 1 Economic Indicators Research Department Staff Forecast for 2018 to 2019 (rates of change, percent, unless stated otherwise)

|

|||||

|

|

2017 |

Bank of Israel forecast for 2018 |

Change from the previous forecast |

Bank of Israel forecast for 2019 |

Change from the previous forecast |

|

GDP |

3.3 |

3.7 |

0.3 |

3.5 |

- |

|

Private consumption |

3.3 |

4.0 |

- |

3.5 |

0.5 |

|

Fixed capital formation (excluding ships and aircraft) |

3.1 |

3.0 |

- |

3.5 |

-1.0 |

|

Public sector consumption (excluding defense imports) |

4.3 |

2.5 |

1.0 |

2.0 |

- |

|

Exports (excluding diamonds and start-ups) |

5.7 |

5.5 |

1.5 |

5.0 |

-1.0 |

|

Civilian imports (excluding diamonds, ships, and aircraft) |

6.9 |

6.0 |

0.5 |

4.5 |

-1.0 |

|

Unemployment ratea |

3.8 |

3.3 |

0.2 |

3.4 |

0.3 |

|

Inflation rateb |

0.3 |

1.2 |

0.1 |

1.5 |

0.1 |

|

Bank of Israel interest ratec |

0.10 |

0.25 |

- |

0.50 |

- |

|

a) Annual average of unemployment in the primary working ages (25–64). b) Average CPI reading in the final quarter of the year compared with the final-quarter average in the previous year. c) End of the year. |

|||||

c. Inflation and interest rate estimates

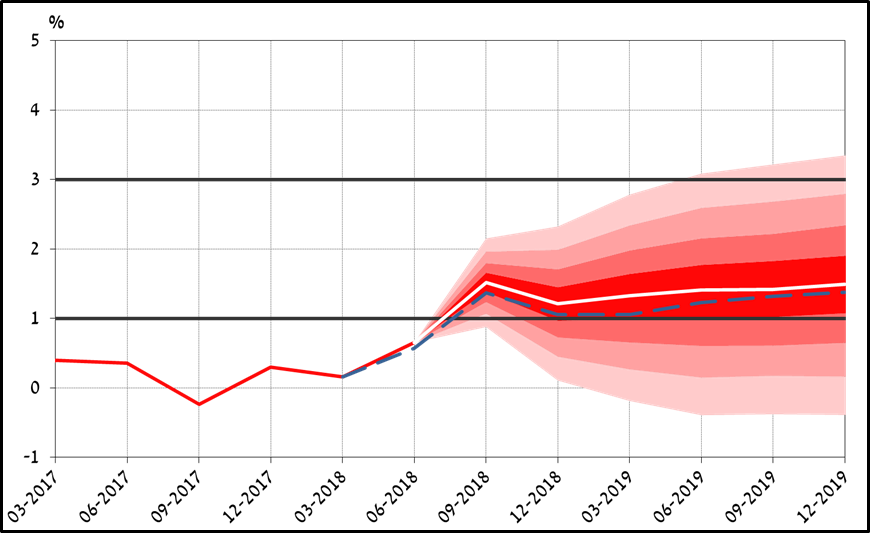

According to the staff forecast, the inflation rate in the four quarters ending in the second quarter of 2019 will be 1.4 percent, inflation at the end of 2018 will be 1.2 percent, and at the end of 2019 it will be 1.5 percent. Inflation in the past four quarters is expected to converge into the target range in the third quarter of 2018. The forecast was revised slightly upward relative to the previous forecast, mainly due to the relative increase in average oil prices in the second quarter of 2018 relative to the average in the previous quarter. This forecast reflects the assessment that inflation will increase moderately toward the center of the target range. The main contribution to inflation is expected to come from the tight labor market, which has been reflected in wage increases for a number of years, although the wage increases have only been translated into an increase in the GDP labor share since 2017, and are therefore now contributing to an increase in inflation. In contrast, the continued increase in competition and measures taken by the government to lower the cost of living are expected to continue to moderate the pace at which inflation converges to the center of the target.

In our assessment, the prices of nontradable goods and services are expected to continue making a positive contribution to inflation, and in particular we assume that the rents item will continue to make a positive contribution. The pace of increase in the prices of tradable goods is expected to rise due to the increase in inflation globally, particularly the increase in energy prices, assuming that the shekel’s exchange rate remains relatively stable. However, the prices of tradable goods are expected to continue increasing at a pace slower than the prices of nontradable goods, further to the long-term price trends in the prices of tradable goods, and due to structural processes (including government measures to reduce the cost of living and the development of Internet commerce).

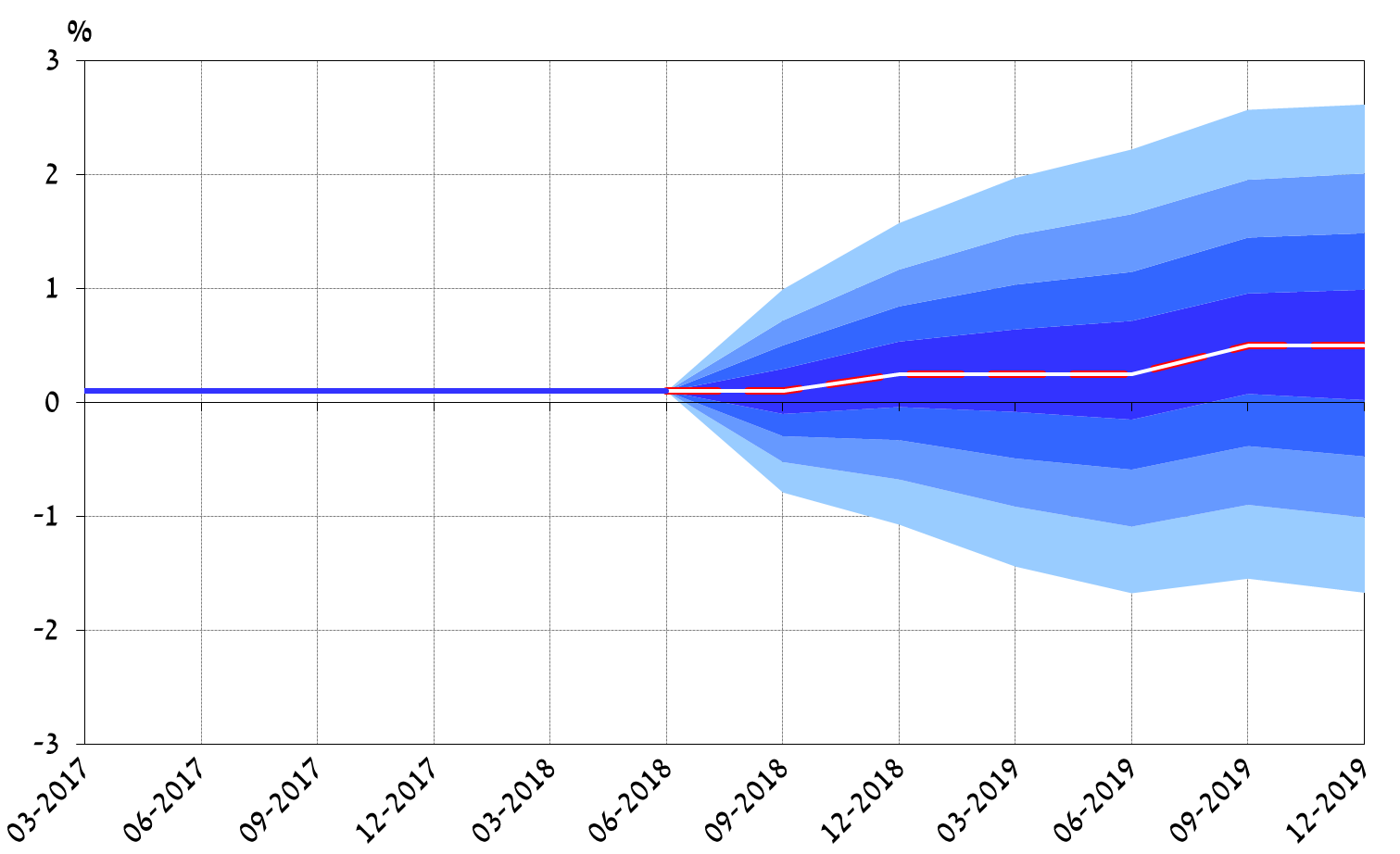

According to the Research Department’s assessment, the Bank of Israel interest rate is expected to start increasing in the fourth quarter of 2018, to 0.25 percent. An increase at that time is consistent with the Monetary Committee’s forward guidance, assuming that the Research Department’s inflation forecast comes to pass. In particular, the Research Department’s assessment is that the annual inflation rate will be within the target range in the third quarter, and that inflation expectations at that time will also be within the target range. According to the forecast, a further increase in the interest rate, to 0.5 percent is expected in the third quarter of 2019.

Table 2 |

|||

Inflation and interest rate forecasts for the coming year |

|||

|

(percent) |

|||

|

|

Bank of Israel Research Department |

Capital marketsa |

Private forecastersb |

|

Inflation ratec |

1.4 |

1.5 |

1.0 |

|

(range of forecasts) |

|

|

(0.7–1.9) |

|

Interest rated |

0.25 |

0.35 |

0.27 |

|

(range of forecasts) |

|

|

(0.10–0.50) |

|

a) Average following publication of the Consumer Price Index for May. Inflation expectations are seasonally adjusted. b) The forecasts published following the publication of the Consumer Price Index for May. c) Inflation rate in the coming year. Research Department: average CPI reading in the second quarter of 2019 compared with the average in the second quarter of 2018. |

|||

|

d) The interest rate one year from now. (Research Department: in the second quarter of 2019.) Expectations from the capital market are based on the Telbor market. |

|||

Table 2 indicates that the forecasts compiled by the Research Department regarding inflation are higher than the projections of private forecasters, but for the first time in a long time, it is close to the expectations derived from the capital market, after the latter increased following the publication of the CPI for May. The Research Department’s forecast regarding the interest rate in one year is similar to the projections of the private forecasters, and lower than the expectations derived from the capital market, after the latter increased markedly in the past two weeks. However, while the assessment of the Research Department is that the next interest rate increase will take place in the fourth quarter of 2018, the average of the professional forecasters and expectations from the capital market attribute greater likelihood that the increase will take place only in the first half of 2019.

d. Main risks to the forecast

Several factors may lead to the domestic economy developing differently than in the baseline forecast. These include uncertainty concerning the future development of the exchange rate; uncertainty concerning the extent to which government measures to reduce the cost of living will roll over to prices and regarding the strength of further measures of this kind that the government may take; uncertainty in quantifying the increase in competition in the economy and regarding the strength of the increase and its continued effect; and uncertainty regarding the direction and intensity of the effect of the cooling off of the housing market on rental prices.

Regarding the global environment, while the growth forecast and world trade forecast are high, recent developments in world trade may worsen to the point of a trade war that may have a significant impact on the Israeli economy, which is small and open.

Figures 1 to 3 present fan charts around the inflation rate, interest rate and GDP growth forecasts. The center of the fan (the white line) reflects the Research Department’s staff forecast. The broken line represents the baseline forecast from the previous quarter. The width of the fan does not reflect a judgmental assessment of the risks to the forecast or their distribution, but is derived from the estimated distribution of the shocks in the Research Department's DSGE model. The fan encompasses 66 percent of the expected distribution.

Figure 1

Actual Inflation and Fan Chart of Expected Inflation

(Cumulative increase in prices in the previous four quarters)

Figure 2

Actual Bank of Israel Interest Rate and Fan Chart of Expected Interest Rate

Figure 3

Actual GDP Growth Rate in the Past Four Quarters and Fan Chart of Expected Growth Rate

(Total GDP over the past four quarters relative to GDP in the preceding four quarters)

Regarding GDP growth (Figure 3), until March 2018, the dotted line reflects the data and estimates that were known at the time when the previous forecast was formulated, while the solid line reflects the updated data and estimates (the difference between them derives from new data and revisions to the data by the Central Bureau of Statistics).

[1] The forecast was presented to the Monetary Committee on July 8, 2018 during its meeting prior to the decision on the Bank of Israel interest rate reached on July 9, 2018.

[2] An explanation of the macroeconomic staff forecasts compiled by the Research Department, as well as a review of the models on which they are based, appear in Inflation Report number 31 (for the second quarter of 2010), Section 3c.

[3] A Discussion Paper on the DSGE model is available on the Bank of Israel website, under the title: “MOISE: A DSGE Model for the Israeli Economy,” Discussion Paper No. 2012.06.