Red Book (hebrew)

Red Book (hebrew)

Pursuant to the Payment Systems Law, 5768-2008, one of the functions of the Bank of Israel is to regulate the economy’s payment and settlement systems, which are critical infrastructures for all economic activity, with the goal of maintaining their stability and ensuring their efficiency. Under this authority, the Bank of Israel continued to act to improve the efficiency and stability of the payment systems in 2015 and 2016. The Bank acted to encourage the use of advanced and lower-risk electronic means of payment and increased its activity in the area of payment and settlement system regulation with the goal of ensuring their stability. Likewise, the Bank acted to enhance competition in the payment systems and to make them more accessible to payment service providers that are not banking corporations.

Among the most significant reforms in recent years is the switch from physical to electronic clearing of checks, in accordance with the Electronic Check Clearing Law, 5776-2016. The law makes it possible to switch from physical to electronic clearing of checks. In the first stage, beginning November 8, 2016, interbank clearing became possible for checks deposited via cellular application. The Electronic Check Clearing Law significantly advances the check clearing process, supports processes of increasing efficiency being adopted by the banking system and enables bank customers to deposit checks electronically, in an advanced, convenient, and efficient manner.

The activity of the National Payments Council headed by the Bank of Israel’s Director General, Mr. Hezi Kalo, was expanded in the past year in order to bring the market in line with regulatory and technological developments, through collaboration of all the entities involved in the sector. The Council’s responsibility is focused on two functions: (1) supporting the attainment of stability and efficiency in the payment systems in Israel; (2) promoting the use of advanced means of payment and enhancing competition in the payment services sector.

In March 2014, the Joint Committee for Promoting Advanced Electronic Means of Payment was established, headed by the Director of the Accounting, Payment and Settlement Systems Department at the Bank of Israel, Mrs. Irit Mendelson. The Committee was set up among other things in accordance with the recommendations of the Locker Committee, whose goal was to reduce the shadow economy in Israel.[1] The Committee for Advanced Means of Payment examined how to promote the use of advanced means of payment, including digital checks and electronic wallets, and published an Interim Report in November 2015. The Committee was of the opinion that the use of advanced means of payment in Israel’s payment system is to be promoted through a coordinated process, including regulation of the technological, legal, and consumer-oriented infrastructures. The Committee’s main recommendations were:

1) To examine the need to set up a central clearing infrastructure and secure national communication infrastructure to execute payments via advanced means;

2) To formulate a legislative memorandum for regulation of payment services, a payment account, and clearing and issuing services;

3) To bring the existing legal infrastructure in line with activity through advanced means of payment;

4) To advance an infrastructure at payment terminals (POS) that will allow contactless transactions;

5) To examine the digital check transaction execution chain;

6) To advance consumer education and the creation of consumers’ confidence in advanced means of payment.

The Bank of Israel is leading the implementation of the recommendations of the Committee for Advanced Means of Payment on several levels:

1) It is carrying out a comprehensive examination of Israel’s market needs in a central retail infrastructure and the situation worldwide, as well as the digital check transaction execution chain.

2) It set up a joint subcommittee to regulate payment services, which compiled principles for regulating payment services and published them for public comment in October 2016; a legislative memorandum is in an advance phase of preparation.

3) It appointed a team to examine the need to set up an additional payment-card switch. The team published its final report in August 2016. The team recommended adopting measures that will remove existing barriers in the market and will allow new entities to join it. This step is an important pillar in opening the payment card market to competition.

4) It set up a Payment Card Committee that defines and regulates the execution of payment card transactions: The principles for development of a protocol for payment card transactions in Israel’s market have been defined; principles were published that establish that the access terms to the Masav (ACH) and Shva systems must be objective, risk-based, transparent to the public, and allow fair and open access to participation in the payment systems.

5) Published regulation related to contactless transactions.

6) In 2015–16, the Bank of Israel collaborated on a comprehensive reform of the regulatory and legal basis that will allow opening essentially all financial services to competition and the entry of new participants in the market and in the payment and settlement system, all in a secure manner that does not risk the existing infrastructure: a Bill to Enhance Competition and Reduce Concentration in the Banking Sector in Israel (Amendments); the Oversight of Financial Services (Regulated Financial Services) Law, 5776-2016; as well as amendments aimed at regulating credit and deposit services, and the activity of P2P online intermediation platforms.

The Bank of Israel is accompanying the process of technological revolution in Israel’s means of payment sector, with an understanding of the importance of regulation in order to ensure the realization of the advantages incorporated in them and to minimize the risks along the way, while maintaining the stability and efficiency of the payment systems in Israel.

Statistical data and main developments in the Payment Systems:

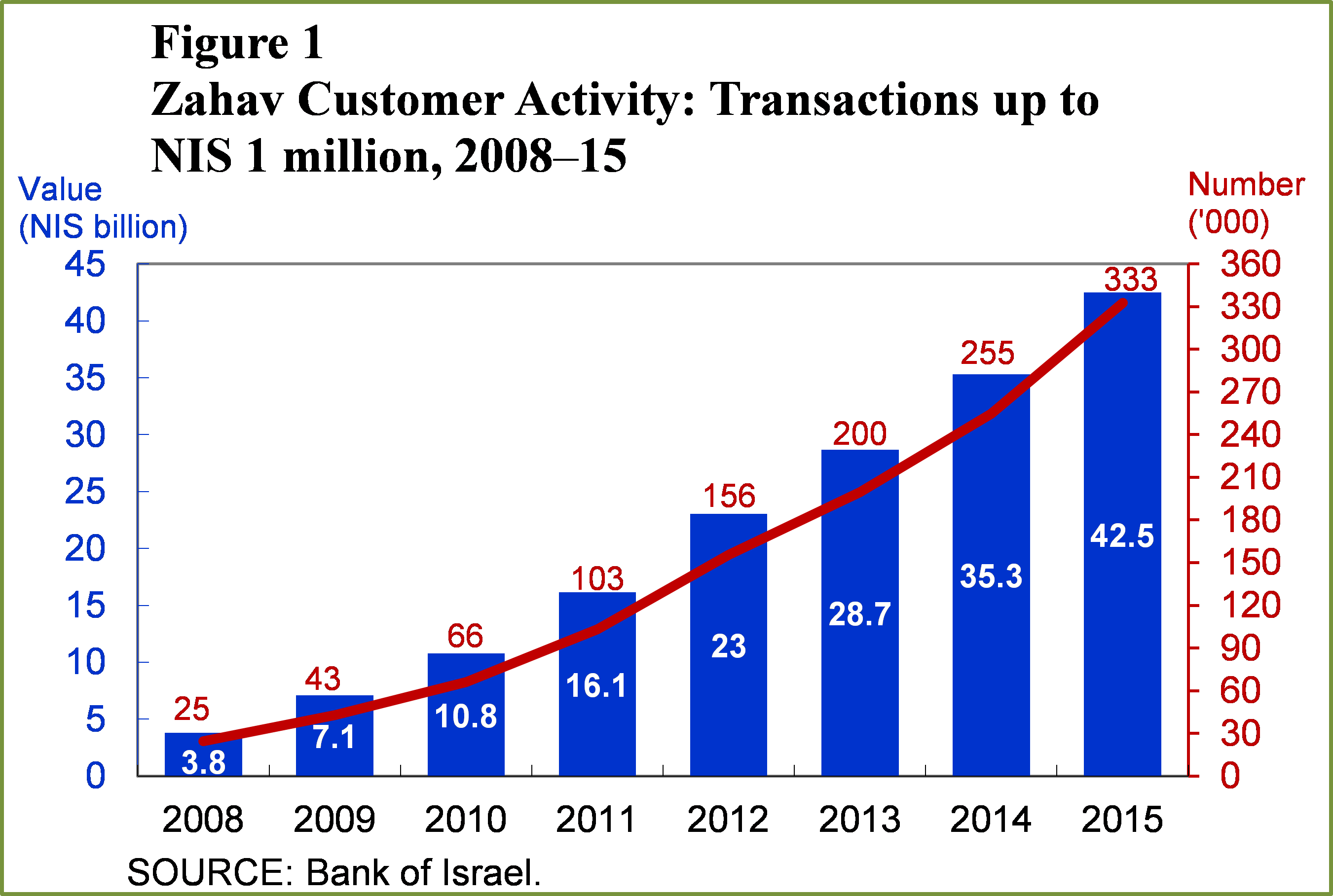

The Zahav (the Hebrew acronym for RTGS) system settles interbank transactions, provides final settlement for clearing houses, and settles transactions initiated by the Bank of Israel. Interbank transactions are those executed by banks and their customers, including transfers from abroad. The Zahav system serves as a clearing house for clearing houses, providing net settlement for clearing houses—Masav (ACH), the Paper-based (Checks) Clearing House, and the Tel Aviv Stock Exchange clearing houses (the Securities Clearing House and the Maof (Derivatives) Clearing House). In 2015, about 603,000 transactions, with a total value of NIS 96,000 billion, were settled through the Zahav system. Compared with 2014, the number of transactions increased by 17.3 percent (514,000) and their total value increased by 21.6 percent (about NIS 79,000 billion), so that the average transaction amount increased by about 3.6 percent.

Figure 1 focuses on customer transactions of up to NIS 1 million, and indicates that there was an increase in the number as well as the value of such transactions. These changes illustrate that the system is beginning to become widespread among households as well as among small and medium sized businesses.

In 2015, transactions by CLS Bank, which carries out most conversion transactions conducted in Israel in which the shekel is one party, totaled about NIS 1,037 billion, a decline of about 7.3 percent relative to 2014. The number of transactions settled by CLS increased by 2 percent in 2015 compared with 2014.

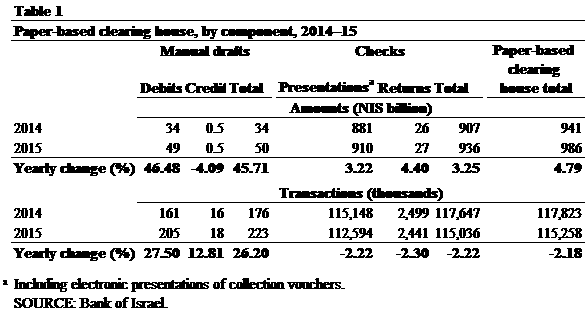

In 2015, Paper-based (Checks) Clearing House activity totaled about NIS 986 billion, compared with NIS 941 billion in 2014, an increase of about 4.8 percent. The number of transactions declined by about 2.2 percent—from about 118,000 to around 115,000.

Electronic credits and debits are executed on the Masav system. The total value of debits on Masav increased in 2015 by about 5.6 percent (compared with an increase of 12.5 percent in 2014), and the total value of credits increased by 5 percent (compared with an increase of 3.5 percent in 2014). There are 28,071 institutions participating in Masav, including banking corporations, the Postal Bank, government ministries and public institutions, as well as other clearing institutions.

The TASE clearing houses settle the results of stock exchange trading. Securities are settled on the TASE clearing houses immediately after the funds are settled between TASE members in the Zahav system.

Similar to most stock exchanges worldwide, trading volume on the domestic stock exchange increased in 2015. Average daily trading volume increased in 2015 to around NIS 1.45 billion (an increase of 19.5 percent vis-à-vis the previous year).

|

Securities trading volumes, 2006–15, Value (NIS billion) |

||||||||

|

Stocks and convertibles |

Government Bonds |

Other Bonds |

Total Bonds |

Makam |

Total |

|||

|

2006 |

360 |

356 |

68 |

424 |

198 |

982 |

||

|

2007 |

506 |

636 |

165 |

801 |

207 |

1,514 |

||

|

2008 |

481 |

761 |

224 |

985 |

192 |

1,658 |

||

|

2009 |

423 |

789 |

223 |

1,012 |

160 |

1,595 |

||

|

2010 |

498 |

579 |

218 |

797 |

291 |

1,586 |

||

|

2011 |

422 |

703 |

217 |

920 |

287 |

1,629 |

||

|

2012 |

264 |

748 |

247 |

995 |

155 |

1,414 |

||

|

2013 |

286 |

810 |

249 |

1,059 |

141 |

1,486 |

||

|

2014 |

297 |

774 |

249 |

1,023 |

157 |

1,477 |

||

|

2015 |

355 |

751 |

255 |

1,006 |

125 |

1,485 |

||

|

Yearly change (%) |

19.45 |

-2.96 |

2.29 |

-1.68 |

-20.55 |

0.57 |

||

The English translation of the full document will be published in the coming weeks.

[1] The Locker Committee recommendations indicated, among other things, that in parallel with reducing the use of paper-based means of payment (cash and anonymous checks), there is a need to create advanced digital alternatives to them. The legislative process of a Cash Law has not yet been completed, but the Bank of Israel is promoting the implementation of the recommendations related to its areas of responsibility.