- The price of homes purchased by salaried first-time homebuyers increased more rapidly than the buyers’ disposable income between 2002 and 2012. As a result, the number of working years necessary for a household to purchase a home increased.

- The rate of home ownership among those aged 25–40 declined during the examined decade.

- First-time homebuyers, at all income levels, purchased larger homes over the reviewed period.

- The share of homes purchased in the periphery increased in recent years, both among first-time homebuyers and among other buyers. This development took place to the same extent in all financial statuses of first-time homebuyers, and is consistent with the relative increase in home prices in the center of the country.

- The median age of first time homebuyers increased by 1–2 years between 2002 and 2012, reaching about 32. The increase occurred among buyers belonging to the upper deciles of the distribution of wage income.

In recent years, home prices in Israel have increased rapidly, while households’ disposable income has increased more slowly. This review assesses various aspects of home purchase affordability. It focuses on young couples—which are defined in this survey as households purchasing a home for the first time—since they are more exposed than others to increases in home prices.[1] In contrast to those upgrading their home, first-time homebuyers do not own a home, and are therefore not protected—even partially—from price increases such as those that have taken place since 2008. In addition, their income is lower, on average, than that of households that own a home, and they have higher child care expenses.

The database upon which the analysis is based was created by merging the residential home transactions file (real estate price file) and a random unidentified sample of 10 percent of salaried employees and their spouses, which contains information on their salaries and main demographic characteristics. These two sources of information were obtained from the Israel Tax Authority, and made it possible to reliably assess the characteristics of homebuyers at a high level of detail. While the sample of salaried employees does not include information on households without wage earners, those that are self-employed, or income from capital and transfer payments, the vast majority of households purchasing a home have income from wages, and income from capital and transfer payments constitutes only a small part of their total income. In addition, the database lacks detailed socio-demographic information and information on how the home purchase is financed.

The first part of the survey presents purchase affordability among the young couples. The second part assesses the differences in affordability between young couples of different financial status. The third part expands the concept of affordability that appears in the first section—relating to the size of the home, its location, and the age of the buyer—and based on this concept, it analyzes purchase affordability among young couples.

1. Purchase affordability among young couples

One of the ways to measure home purchase affordability is by the median number of years of disposable income that are necessary for a household to purchase their residence.[2] Accordingly, we will describe the households that are at the focus of this survey, the development of their income, and the prices of the homes they have purchased. We will then present the affordability index that is derived from this.

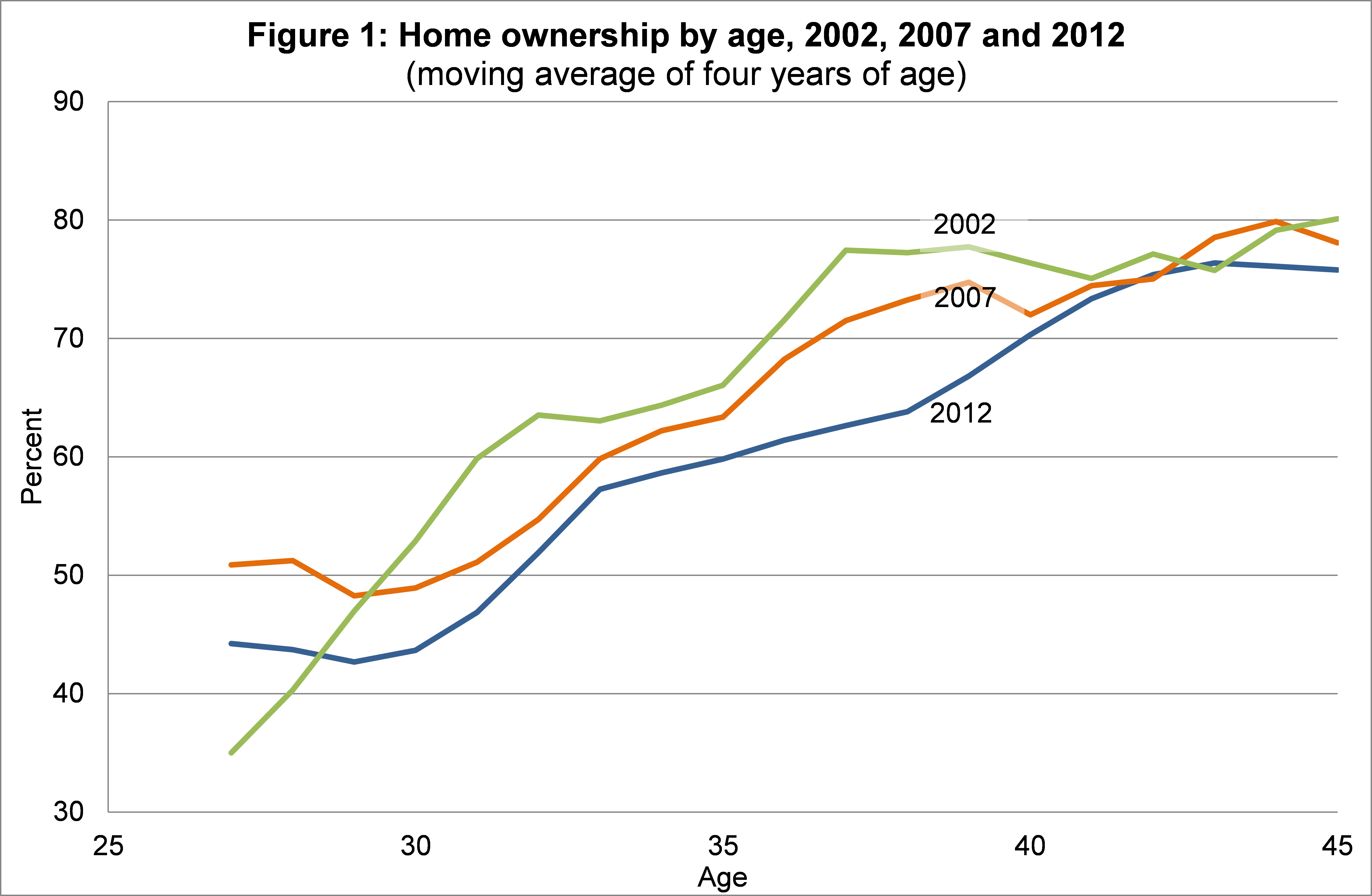

The young couples—which here include, as mentioned, the households purchasing a home for the first time—constitute about one-third of homebuyers. According to the Central Bureau of Statistics Household Expenditure Survey, the percentage of young households that own a home declined in the examined decade. By way of illustration, and as shown in Figure 1, in 2002, about 66 percent of 35-year-olds surveyed owned a home, and in 2012, that percentage had declined to about 60 percent.

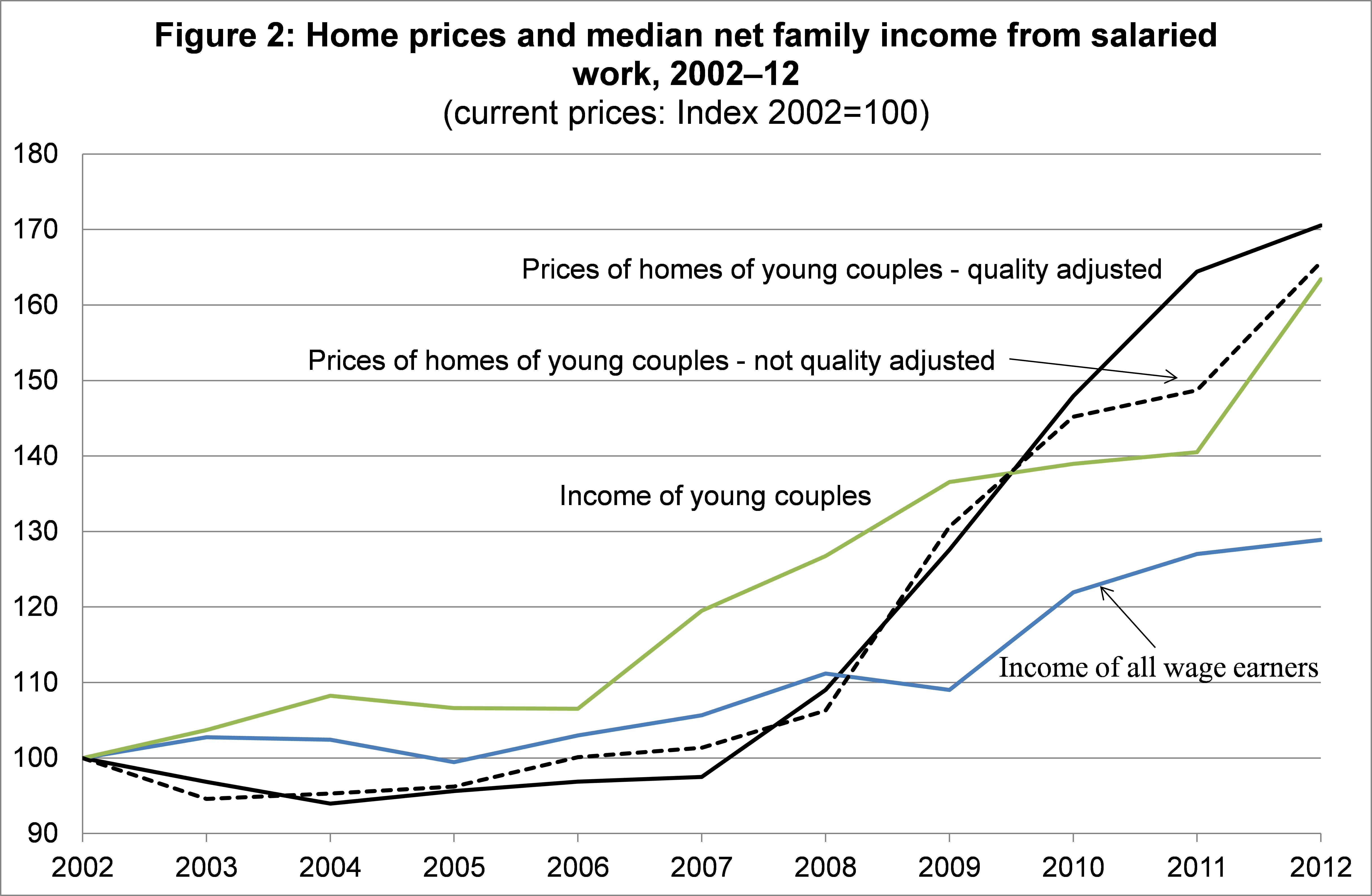

Regarding the income of young couples from salaried employment, the median net monthly family income[3] increased by about 63 percent in nominal terms during the reviewed period, while among all salaried employees, it increased by about 29 percent (Figure 2).[4] The gap is the result of the fact that homebuyers are highly represented among salaried employees with good financial status, and over the years the wages of this group increased more rapidly than that of all salaried employees, particularly since 2007. This phenomenon shows that the income of households that expanded—due to marriage and birth—increased more rapidly than the income of other households.[5] In addition, the salaries of first-time homebuyers in all decile groups increased more rapidly than the general average of the young wage earners in each group, a phenomenon that attests to the strengthening of the financial status of the buyers, relative to those who did not buy a home.

The prices of homes purchased by young couples, after adjusting for quality[6] (meaning after taking into account characteristics such as the size and location of the home), increased by an aggregate of about 72 percent during the surveyed period, and the increase took place—almost completely—from 2008 onwards. It should be noted that until 2010, raw home prices moved in tandem with quality-adjusted home prices—evidence of the fact that on average the quality of the homes purchased by young couples during this period did not change. In 2011, there is a deviation from the trend, which shows that the quality of the homes declined. But it seems that in 2012, there is a correction and a return to the same home quality.

Purchase affordability—the median ratio between the price of homes purchased by young couples and the number of years of disposable income of those couples—improved between 2002 and 2008 from 6.1 to 5.1 years. In the following two years, it declined sharply—with the increase in home prices—and then stabilized at about 6.4 years (Figure 4 below).

2. Differences in affordability between young couples of different financial statuses

In order to assess the home purchasing patterns by financial situation, we attributed the households to deciles by disposable income from salaried work per equivalized individual in all households (including those that did not purchase a home). It should be emphasized that this is income from salaried work during the current year, and not income over the life cycle. Therefore, the lower deciles also include salaried households with income during the current year that, while low, will increase in the future (for instance, young people at part-time or temporary jobs). The results are not sensitive to the way in which the population was divided into decile groups.

Figure 3 shows the portions constituted by the various deciles among young couples in 2002 to 2012.[7] The top three deciles are over-represented among homebuyers: While their share of the salaried population is 30 percent, among homebuyers it comes close to 50 percent. In parallel, the two lowest deciles are under-represented, constituting just 10 percent of homebuyers. (In total, just 1 percent of households in these two deciles purchase homes in any year.) The distribution of home purchases by deciles was relatively stable until 2009. Thereafter, an interesting phenomenon took place: Even though purchase affordability declined among the intermediate deciles, their share of total purchasers increased by a not-inconsiderable amount—about 5 percentage points—at the expense of the share of purchasers from the upper deciles. A possible explanation of the change in trend concerns the easy terms of financing of the mortgages taken out during that period: It is possible that among the intermediate deciles, these terms were a very significant consideration in the decision to purchase a home.

Figure 4 shows that there is a negative correlation between income and the median number of years of net income required for young couples to purchase their home. It should be remembered that even though transfer payments between individuals (for instance from parents to children) in many cases—and apparently in all deciles—serve as a source of financing for the purchase of a home, there is no reliable information in Israel on such transfers, which are apparently one of the factors explaining how the median number of years of income in the lower deciles can be so high.[8] The index of purchase affordability among young couples is similar to the index among all salaried buyers, although the income of the former is lower. As we will later see in detail, this means that young couples purchase relatively inexpensive homes—both smaller and located in less desirable areas.

Since 2009, there has been a decrease in purchase affordability among young couples, particularly in the intermediate deciles: While 5.8 years of income were required for a purchase in 2008, 7.6 years were required in 2012, an increase of 30 percent. In contrast, the upper deciles required 4.5 years and 4.9 years respectively, in order to finance the purchase of a home—an increase of 9 percent. In other words, purchase affordability declined to a greater extent among the intermediate deciles.

3. Purchase affordability among first-time homebuyers by the expanded affordability concept

As mentioned, in the first part of the survey, we measured purchase affordability by the median number of years of disposable income necessary for a household to purchase its home. However, this index does not take into account additional aspects of the ability to purchase a home. By way of illustration, the price of a home is dependent on its physical characteristics (size, age and so on), and its location relative to high demand areas. When homebuyers compromise on the physical characteristics or location of the home in order to lower its price, it basically constitutes a worsening of affordability. The same is true of a delay in the timing of the purchase due to a lack of means with which to finance it. These aspects are the focus of the third part of the survey.

However, before turning to these aspects, another very important aspect of the ability to purchase a home should be emphasized—the burden of financing, both through a mortgage and through equity, including transfers from other individuals (such as from parents to children). Friedman and Ribon (forthcoming) researched this aspect based on the Household Expenditure Surveys, and did not find any growth in recent years in the share of mortgage repayments out of disposable household income. This finding is explained by some increase in equity, a decline in the average interest rate on mortgages, the extension of the repayment period, and some increase in real household income.

Size of the home

Estimations[9] show that the area of the homes (in square meters) purchased by young couples from the upper deciles was about 11 percent larger than those purchased by young couples from the intermediate and lower deciles, and the number of rooms was 8 percent larger. Over time, there was a slight increase in the size of the home, but there were no differences between the deciles from this standpoint. Home area per person increases with income— increasing by about 10 percent between 2002 and 2012, because the area of the home increased and the number of people in the household decreased. Home area per person increased in the intermediate deciles more rapidly than in the upper deciles. These trends show that even though purchase affordability declined in recent years, particularly among the middle class, the physical residential conditions of young couples who purchased a home did not worsen, and developed similarly to the conditions for all homebuyers.

Location of the home

The quality of housing services depends, inter alia, on the location of the home. Where home prices increase, some households that would prefer to reside in high-demand areas—particularly households with limited means—are forced to find a housing solution in a more distant location. This phenomenon may be evidence of worsening purchase affordability, and may lead to a deepening geographic separation by income levels.

Home prices throughout Israel developed differentially during the surveyed period: Prices (adjusted for quality, in accordance with the Central Bureau of Statistics definitions) in the center increased by an aggregate amount of 95 percent, while those in the periphery increased by 70 percent.[10]

Home prices in the center increased, therefore, at a more rapid pace than home prices in the periphery. Alongside this, from 2010 onwards, first-time homebuyers in the periphery increased as a share of all first-time homebuyers, from about 20 percent in 2009 to about 25 percent in 2012.[11] A similar phenomenon took place among all salaried homebuyers. However, in most districts, there was no material change in the mix of deciles of first-time homebuyers. A similar picture emerges when looking at the mix of deciles of first-time homebuyers within neighborhoods of various socio-economic rankings.[12]

In general, home prices are lower the greater the distance from Tel Aviv. When estimating the distance between homes purchased by young couples and the city (within a range of up to 30 km from the city)[13], we find that a home purchased by a couple from the highest deciles was, on average, about 10 percent closer to Tel Aviv than a home purchased by a couple from the intermediate and lower deciles. The prices of homes purchased by young couples in Tel Aviv increased by more than 100 percent during the study period, while in the center district, they increased by 85 percent. In contrast, there was only an insignificant increase over time in the average distance from Tel Aviv, and there were no differences between statuses from this standpoint.

In summation, between 2002 and 2012, the rate of homes purchased by young couples in the periphery increased, but this rate did not change relative to total buyers. Furthermore, there was no evidence of a deepening geographic separation between the income deciles among young couples.

Purchase age

Another aspect of purchase affordability is the age at which a home is purchased for the first time. The median age increased during the reviewed period by 1–2 years, and reached about 32—due to the increase in the purchase age in the upper deciles—while the median marriage age increased by less than one year (and by about one year among the upper deciles), and the salaried employee population group almost did not age. This means that the age at which a home is purchased increased in the upper deciles and did not change in the intermediate deciles, even after adjusting for the increase in the age of marriage and the aging of the salaried population. It should be noted that the timing of marriage may be affected by young couples’ ability to purchase a home.

[1] For more on this issue, see Friedman, Y. and S. Ribon (forthcoming), “Whence the money?—Home purchases and their financing: An analysis using Household Expenditure Survey data, 2004–2011”, Bank of Israel; Bank of Israel (2014), “Housing affordability: Home prices and rents across districts in Israel, 2004–2012”, in Recent Economic Developments, 137, October 2013 to March 2014; Ben-Naim, G. (2012), “First-time homebuyers in the past decade—characteristics and trends”, Israeli Tax Quarterly, 131 (33), pp. 63–83 (in Hebrew).

A discussion on rental affordability can be found in Bank of Israel (2014), and in Brender, A. and M. Strawcyznski (2014) “Government Support for Young Families in Israel,” Bank of Israel, Discussion Papers Series, 2014.02.

[2] As opposed to the custom to use the ratio between the average price of homes purchased and the average income of all households (whether they have purchased a home or not). There is a conceptual discussion of the various measures of housing affordability in Bank of Israel (2014).

[3] The net annual salary of those sampled and their spouses, divided by 12. A distinction should be made between this wage and the wage per employee post. The latter equals the gross wage per month of work, while the wage here takes into account the number of working months in a year. We emphasize that the database identifies the spouse only in a case where the sampled individual is married, while in the Central Bureau of Statistics surveys, the household also includes spouses that are not married (as well as other adults).

[4] The calculation was made on the wages of households that purchased a home for the first time, in the year in which they purchased their home, compared with the wage of all salaried employees in that year, including those who did not purchase a home.

[5] A discussion of the differences between “young parents” and other salaried employees appears in: Brender, A. and M. Strawcyznski (2014).

[6] The changes in home prices were calculated hedonically. This method takes into account the size, age and location of the home, similar to the method used by the Central Bureau of Statistics to calculate the Index of Home Prices (which is not part of the Consumer Price Index).

[7] When examining the distribution of ages of the salaried employees who purchased a home for the first time, we find that after cutting off 10 percent from each side of the distribution—meaning the youngest and oldest people—we are left with an age range of 24–45. Therefore, we calculated the income deciles among salaried employees in this age range (homebuyers and others), and from here on, we will relate only to this group.

[8] It should be remembered that homes for investment purposes are sometimes recorded, for tax considerations, in the name of relatives that earn low wages.

[9] Estimations for the years 2002–2012 of the home area (number of rooms) as a function of the following explanatory variables: dummy variables for deciles, number of people in the household, dummy variables for years, and fixed effect for the community. For some, interactions between the deciles per year were added. Similar estimations of home area per person were also made, in which the number of people was deleted from the explanatory variables.

[10] Ben-Tovim, N., Y. Yakhin, and Zussman, N., (2014), “Measuring home price variation using repeated sales methodology”, Bank of Israel, Periodic Papers, 2014.1

[11] Another factor that may have explained the move to the periphery is the increase in the supply of homes there relative to the center. However, the area of homes, the construction of which was completed in the periphery, compared to the area in the center, remained almost unchanged during the surveyed period.

[12] Since the socio-economic ranking of the neighborhood depends to a great extent on the income of its residents, we used the rating at one point in time—the Central Bureau of Statistics socio-economic ranking for statistical areas according to the 2008 Census.

[13] Estimations for the years 2002–2012 in which the explanatory variables are dummy variables for decile, the number of people in the family, and dummy variables for years. Some of the estimations include interactions between deciles per year.