This press release as a Word document

This press release as a Word document

Tables and Charts of this release in Excel

Tables and Charts of this release in Excel

Tables and charts summarizing development in December

The Bank of Israel's Information and Statistics Department is publishing this month a summary of the developments in the foreign currency market in 2012.

1. The Exchange Rate

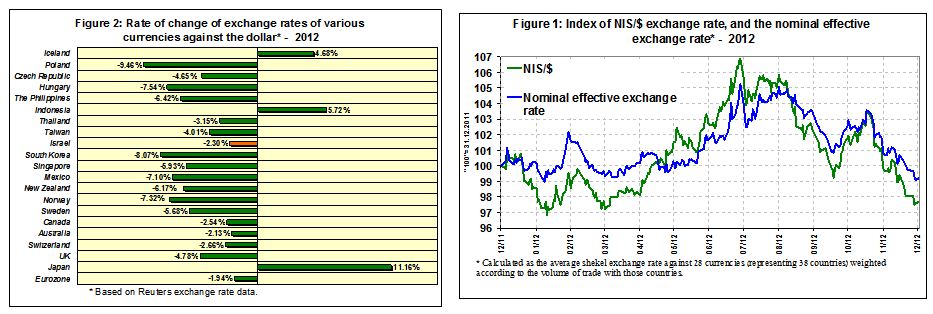

The shekel strengthened against the dollar, as the dollar weakened against currencies worldwide

The shekel appreciated by about 2.3 percent against the dollar and by about 0.4 percent against the euro during 2012. Against the currencies of Israel's main trading partners, in terms of the nominal effective exchange rate of the shekel (i.e., the trade-weighted average shekel exchange rate against those currencies), the shekel strengthened by about 0.8 percent.

The developments in the exchange rate of the shekel against other currencies in 2012 were in line with the major trends in global currency markets—the dollar weakened by about 2.7 percent against the Swiss franc, by about 2 percent against the euro, and by about 4.8 percent against the pound sterling. The dollar weakened even more against the currencies of most emerging markets (Figure 2).

The exchange rate's trend during the year was not uniform: In April–August, the shekel depreciated against the dollar by about 8 percent, as the dollar strengthened worldwide, and against the background of geopolitical tension. Beginning in September, the dollar weakened worldwide and the geopolitical tension eased. This contributed to a change in the trend of the shekel-dollar exchange rate, which appreciated by about 7 percent during the last third of the year.

2. Exchange Rate Volatility

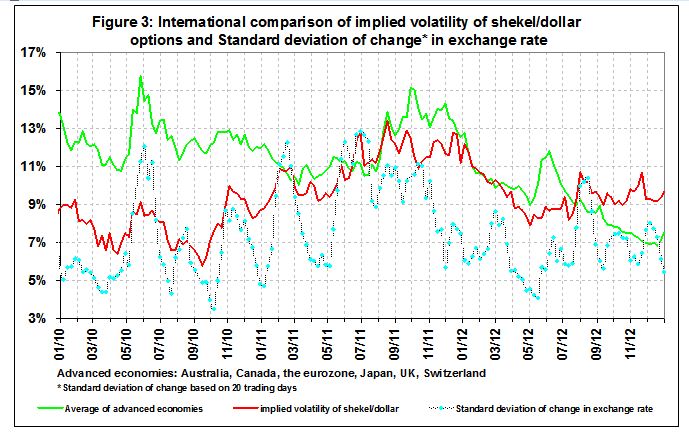

Actual volatility as well as implied volatility of the exchange rate in shekel/dollar options declined

The monthly standard deviation of changes in the shekel-dollar exchange rate, which represents its actual volatility, declined in 2012 by about 2 percentage points, to 5.5 percent in December, following an increase of about 2.5 percentage points in actual volatility during 2011.

The average monthly level of the implied volatility in over the counter shekel-dollar options—an indication of expected exchange rate volatility—declined during 2012 by about 2.7 percentage points, to about 9.4 percent, following a sharp increase of about 8 percentage points in expected volatility from the end of 2010 through the middle of 2011.

An examination of the year itself indicates the marked differences between the two halves. In the first half, there was a continued decline in expected volatility, with a mixed trend in actual volatility. In contrast, in the third quarter of 2012, the increase in actual and expected volatility resumed, an increase which apparently indicates a rise in the level of uncertainty regarding the shekel's exchange rate. In contrast, there was continued decline in the expected volatility of advanced economy exchange rates against the dollar.

It should be noted that from a historical perspective, although implied volatility is generally higher than actual volatility, the latter is more volatile and ranges considerably when there are economic events which impact on the exchange rate (Figure 3).

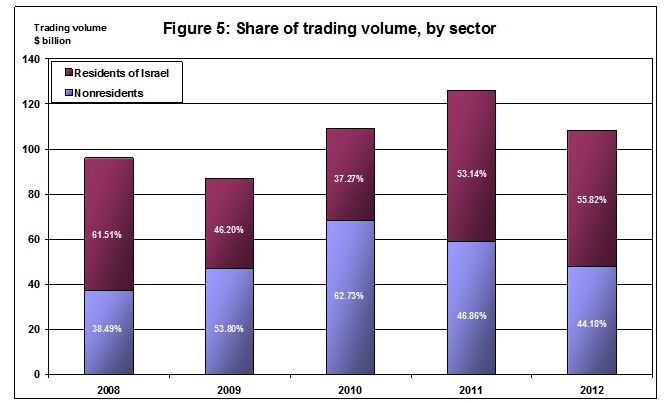

3. The Volume of Trade in the Foreign Currency Market

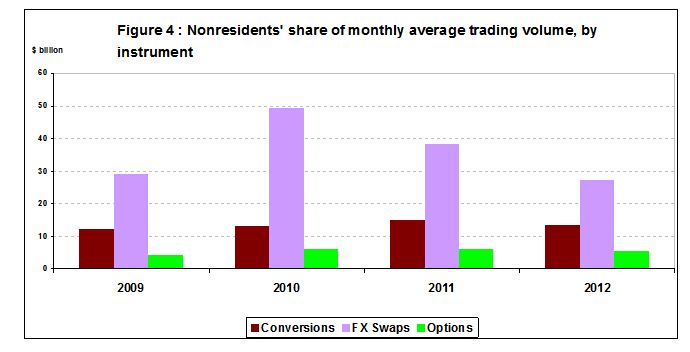

During 2012, there was a sharp decline in average monthly trading volume and in nonresidents' share of trading volume.

The average monthly foreign currency trading volume during 2012 was about $110 billion, a decline of about 14 percent compared with 2011, following a marked increase in trading volume in the foreign currency market during 2010 and through the first half of 2011. Most of the decline in volume was concentrated in swap transactions, where there was an average decline of about 18 percent, to an average monthly level of about $60 billion in 2012 (Figure 4).

The average volume of conversions (spot and forward transactions) declined more moderately during 2012 to $37 billion per month, and options transactions declined moderately to $10 billion per month on average.

Nonresidents' share of total trade declined this year by about 2.7 percentage points to about 44 percent, following a decline of some 25 percentage points during the second half of 2011. The decline in nonresidents' share of total trade occurred against the background of steps taken by the Bank of Israel and the Ministry of Finance in the foreign currency market in 2011: Imposing a reserve requirement on futures and swap transactions, and cancelling nonresidents' tax exemption on makam. The decline was concentrated in nonresidents' swap transactions and reflected the exit from the makam market at the same time as the contraction of swap positions.

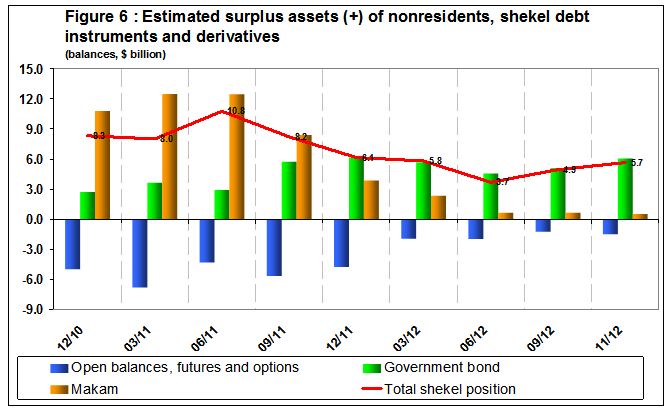

4. Changes in nonresidents' shekel exposure in debt instruments

The estimate of surplus assets over liabilities in shekels in debt instruments (shekel exposure) decreased from the middle of 2011 until the middle of 2012 by about $7 billion, to a level of $4 billion. The decline in exposure reflects marked realizations by nonresidents in makam which totaled, from the middle of 2011, about $10 billion, and which were partly offset by a decline in the surplus future shekel liabilities in derivative instruments (Figure 6).

Beginning from the second half of 2012, there were renewed net investments by nonresidents in government shekel bonds, and there was a moderate increase in shekel exposure, which was $5.5 billion at the end of November.