![]() To the press release as a Word document

To the press release as a Word document

- The weighted inflation forecast is based on a weighting of five forecasts that are formulated at the Research Department. While the previous method was calculated as a simple average assigning each of the forecasts an identical weight, the new method assigns each forecast its own unique weight, including a negative weight for one of them.

- The use of a negative weight makes it possible to exploit the high positive correlation between the deviations of the Research Department’s forecasts, and thereby reduces the errors in the weighted forecast.

- Starting in January 2013, the new weighted forecast has been presented to the Monetary Committee in its discussions on formulating monetary policy.

- The new weighting method should also improve projections of other economic variables, thereby improving forecasting in other areas.

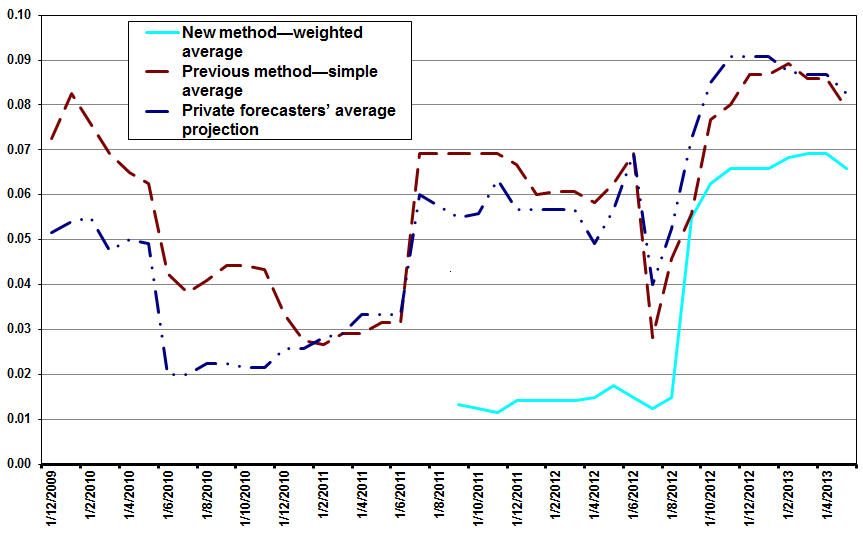

The Bank of Israel Research Department has adopted a new method for weighting inflation forecasts, following a study conducted by Dana Flikier of the Research Department. The research studies the monthly forecasts of the change in the Consumer Price Index in the coming month prepared by the Research Department, and assesses what the best method is for weighting them into a unified forecast. It proposes a new weighting method, which significantly improves (by about 50 percent) the precision of the weighted inflation forecast. Starting in January 2013, the new weighted forecast has been presented to the Monetary Committee, enabling it to improve the decision-making process concerning monetary policy measures. The forecasts serve the bank’s internal discussions, and are not published.

The Research Department compiles the forecasts through five separate models. Previously, the Department calculated a simple average of the five forecasts, granting each individual forecast an equal weight. The study proposes a weighting method that takes advantage of the potential inherent in the information on past performance of the forecasts—their level of precision and the correlations between their deviations. The method creates a weighted forecast by assigning each of the models a unique weight, and a negative weight to one of them. The weights given to each model vary from one month to the next in accordance with the information accumulated up to the date on which the forecasts are prepared.

The negative weight assigned to one of the models does not attest to the model providing a completely mistaken inflation forecast. The use of a negative weight makes it possible to take advantage of the high positive correlation between the deviations of the models’ projections (meaning that all of the models generally err in the same direction). It is thus possible to obtain a weighted forecast which is more precise than the forecast that would have been obtained had the model with a negative weight been eliminated from the calculation. Since all of the models generally err in the same direction, assigning a negative weight to one of them (and thus to its deviations from actual inflation as well), makes it possible to minimize the total deviations—the error of the weighted forecast.

The Figure presents the improvement introduced by the use of the new method (weighted average) compared to the previous method (simple average), and relative to the average projection of private forecasters.

* MSE - Moving average over the course of a year

The study presents a methodology implemented both in Modern Portfolio Theory (MPT) and in the literature dealing with the combination of forecasts. It also presents a mathematical and empirical basis for the method that it develops. This weighting method should also improve forecasts of other economic variables and improve the Bank of Israel’s forecasting in other areas.