- Israel’s trade in goods with Middle Eastern countries, long limited, has been growing rapidly in the past two years. Imports from Turkey are surging and so are imports from and via the United Arab Emirates following the Abraham Accords. Israeli exports to these two countries have increased, as have natural gas exports to Egypt and Jordan. Total goods imports from the region’s countries exceed exports to them.

- Israeli tourism to the region’s countries—mainly Turkey, Egypt, and the new destinations of the UAE and Morocco—expanded to more than 1.8 million visits in 2022 and increased relative to 2019 as well. The number of passengers flying to countries in the region (including back to Israel) was 3.9 million in 2022—about one-fifth of international air travelers through Ben-Gurion International Airport.

For decades, Israel developed as an “island economy”, a market cut off from neighboring Middle Eastern countries with the exception of Turkey. Even peace agreements with Jordan and Egypt did not produce economic relations of macroeconomic significance. The Abraham Accords (September 2020), normalizing Israel’s relations with the United Arab Emirates (UAE), Bahrain, and Morocco, and successor agreements such as the Israel–UAE free-trade agreement (May 2021), created expectations of the development of significant economic relations between Israel and countries in the region. These expectations are consistent with public willingness in the Gulf States to maintain relations with Israel, in contrast to disapproval of normalization with Israel in Egypt and Jordan.[1]

This analysis describes the widening of trade relations in goods and tourism[2] between Israel and regional countries in the two years since the Abraham Accords were signed. Whereas trade relations with the UAE have expanded swiftly in the past two years, the main increase in trade took place with Turkey. Concurrently, trade with Egypt and Jordan has grown to a limited extent, mainly as a result of Israeli natural gas exports. In addition, the lifting of COVID-19 restrictions on foreign travel by Israelis in 2021 brought about a rapid increase in the number of Israeli tourists visiting Turkey, the UAE, Egypt, and Morocco. The number of air passengers from Israel to Middle Eastern countries and, via them, to continuing destinations also grew. As a rule, imports of Middle East goods to Israel exceed Israeli exports to these countries, and Israeli tourism to regional destinations far surpassed Middle East tourism to Israel.

Trade in goods

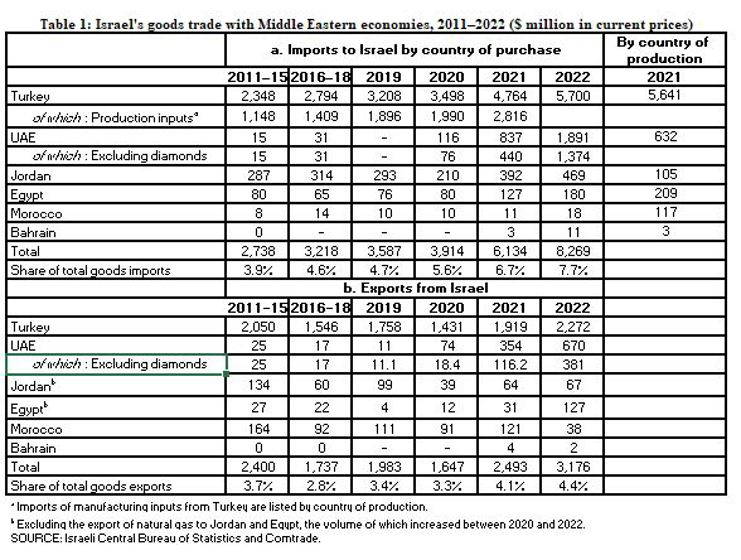

In the decade preceding the Abraham Accords, most of Israel’s trade in goods with regional markets was with Turkey. Trade with Jordan and Egypt, which have had peace treaties with Israel for decades, was limited despite agreements on encouraging this activity, such as the Qualified Industrial Zone accords.[3] Trade with the UAE added up to several tens of millions of dollars per year at the most. In the past two years, trade with the region’s countries has been growing rapidly—particularly with Turkey and the UAE. Goods imports from the region to Israel in 2022 climbed to a record US$ 8.3 billion (7.7 percent of total goods imports) and exports to regional markets increased to US$ 3.2 billion (4.4 percent of goods exports) (Table 1). In addition, natural gas exports to Egypt and Jordan grew to 9.2 BCM.[4]

TABLE 1

Goods Imports

Most of the increase in imports from the region’s countries in 2021–2022 was from Turkey and the United Arab Emirates. Israel also imports hundreds of millions of dollars worth of goods from Jordan, mostly goods produced in other countries. Imports of goods from Egypt and Morocco have grown as well. Much of the imports from Egypt and most of the imports of goods produced in Morocco were imported through other countries (Table 1, compare imports by country of production and by country of purchase in 2021).

The value of imports from Turkey (as the country of purchase) was US$ 5.7 billion, nearly twice the 2019 level. In addition, Israel imported more than US$ 800 million per year in goods produced in Turkey via other trade partners. Most of the increase in imports from Turkey was in production inputs, which grew from 4 percent of Israel’s total import of production inputs in the previous decade to 9 percent in 2020–2021. In general, imports of production inputs from Turkey increased between 2020 and 2022, along with nominal and real growth in total imports of production inputs to Israel, due to the increased global supply chain pressures in the past two years. Goods imported from Turkey to Israel are mainly metals, machinery, plastics, cement products, textiles, and motor vehicles.

Recorded imports from the UAE have been developing rapidly since the Abraham Accords were reached (September 2020), and added up to US$ 1.9 billion in 2022. Imports from the UAE are expected to see further growth in coming years as the countries solidify their business relations and implement their bilateral free-trade agreement. Even if these imports double, however, they will still account for only a few percent of Israel’s imports and an even smaller fraction of the UAE’s exports.

The UAE is an important regional trade hub due to its position along maritime and air routes between Europe, Africa, and Southeast Asia. It provides a modern logistical and financial infrastructure for large-volume international trade, and some two-thirds of Emirati exports (excluding fuel) are goods that are re-exported after having been imported from other countries.[5] This phenomenon stands out in particular in the Emirates’ exports to Israel. According to Emirati data, 82 percent of the UAE’s exports to Israel in January–September 2022 were re-exports of goods imported from elsewhere.[6] Goods imports via the UAE rather than from the countries of production indicates that this trade pattern streamlines the import process and/or lowers its costs, including those of insurance and shipping.

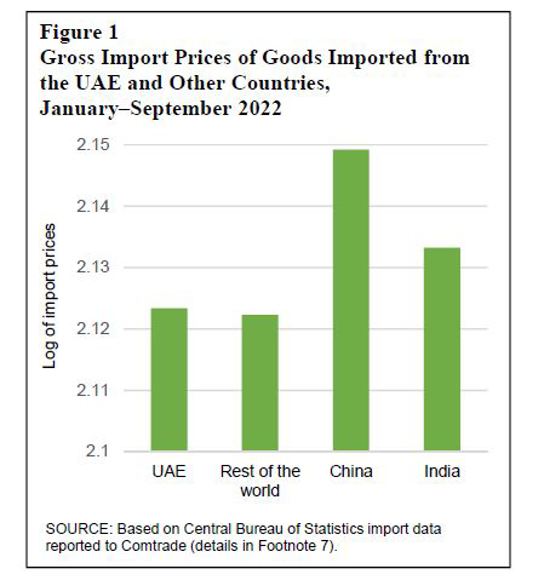

FIGURE 1

By comparing import prices from the UAE with those of parallel goods originating elsewhere, we can examine the advantages of trade via the Emirati trading hub. Gross import prices (including shipping and insurance) of goods (excluding diamonds) that were imported from the UAE in 2022 were 1 percent lower the import prices of the same goods from India, and 2.6 percent lower than from China, respectively. The import prices of the same goods from the rest of the world, however, were slightly lower than the prices of imports from the Emirates (Figure 1). Therefore, importing via the UAE may lower the cost of importing from Southeast Asia slightly but is unlikely to make overall imports to Israel much less expensive.[7] Imports from nearby trade partners, however, may make importation more efficient by shortening delivery times, allowing Israeli importers and manufacturers to maintain smaller inventories in Israel, particularly as the cost of maintaining inventory rises in tandem with the increase in interest rates.

Goods exports

Turkey is Israel’s most important export destination in the region. Exports to Turkey recovered gradually in the last few years after contracting by around one-fourth due to bilateral tension after Operation Protective Edge (2014). Israeli exports to the UAE increased following the Abraham Accords (September 2020), but increased more slowly than imports. Furthermore, more than one-third of these exports are diamonds, which generate relatively little local added value. Reported Israeli exports (excluding gas and water; see below) to other Middle Eastern countries, particularly Egypt and Jordan, came to only several hundred million dollars in 2022, consistent with the negative public sentiment in those countries toward economic cooperation with Israel (see Footnote 1).

Gas and water exports to Egypt and Jordan

In addition to the exports reported above, Israeli exports of gas and water to Egypt and Jordan—Israel’s current export destinations for these goods—have increased and are expected to continue growing in the years to come. Exports of Israeli gas to Jordan grew gradually from 2.1 BCM in 2020 to 2.9 BCM two years later, and gas exports to Egypt increased from 2.2 BCM to 6.3 BCM during those years. Gas exports to these two countries together accounted for 45 percent of total gas produced in Israel’s economic waters in 2022. The expansion and improvement of gas transmission infrastructure, from about 12.5 BCM per year in 2022 to about 22 BCM per year in 2026, is expected to facilitate higher gas exports to these countries.[8] Some of the gas that Egypt imports from Israel is liquefied there and re-exported to Europe. In June 2022, Egypt, the EU, and Israel signed a memorandum of understanding that paves the way to the expansion of Israel gas exports to Europe via Egyptian liquefaction facilities.

In addition to natural gas, Israel has been selling water to Jordan in the past two decades. In accordance with the bilateral peace treaty (1994), Israel undertook to sell Jordan 50 million cubic meters of water at a subsidized price. In October 2021, the two countries signed an agreement for the sale of an additional 50 million cubic meters over a three-year period. In 2021 and 2022, Israel, Jordan, and the UAE also signed memoranda of understanding concerning the Prosperity Project, which focuses on promoting the possibility of Israel’s sale of up to 200 million cubic meters of water per year to Jordan and Jordan’s selling 600 MW per year of electricity from renewable sources to Israel.[9] Imported water from Israel is increasingly important for Jordan, which consumes about 1 billion cubic meters of water per year and faces an ongoing decline in the available quantity of water per resident commensurate with population increase.[10]

Trade in services

Even though most Israeli exports are composed of services, mainly business services, there are so far no indications of sizable trade in services between Israel and other Middle Eastern countries, with the exception of visits by Israeli tourists. The development of trade in goods with and via the UAE, however, is expected to increase trade in transport and financial services that are associated with international trade. The limited scale of trade in nontourism services is typical of trade among most of the region’s markets.

Israeli tourism to Middle Eastern markets expanded in 2022 to a record of more than 1.8 million visits, continuing the increase in visits that began in 2017–2019 and resumed in 2022 after the COVID-19 restrictions on outgoing tourism from Israel were lifted. On top of the growing scale of Israeli tourism to the veteran destinations of Turkey and Egypt, Israeli tourists flocked to new destinations such as the UAE and Morocco.[11] The number of Israeli residents who entered Jordan through the overland border crossings, however, has not yet returned to its prepandemic 2019 level and arrivals of citizens of other Middle Eastern countries remain minuscule.[12]

FIGURE 2

The Abraham Accords also brought with them the establishment of air transport relations between Israel and the UAE and Bahrain, resulting in approximately 1 million passengers among the destinations, as well as the resumption of flights from Israel to Morocco and Sharm el-Sheikh, Egypt. The rapid increase in air travelers to the UAE and via there to Eastern Asia appears to have come at the expense of travelers who land in Jordan and may continue to destinations in the East, which decreased steeply between 2019 and 2022. There were a total of 3.9 million air passengers to regional markets in 2022[13] (20 percent of international air passengers from Ben-Gurion Airport), compared with 2.5 million (11 percent of passengers on these flights out of Ben-Gurion) in 2019. At the beginning of 2023, Israeli airlines resumed service to Turkey and began to fly to destinations in the East over Saudi Arabian and Omani airspace, significantly shortening their air routes to Asia. The strengthening of Israel’s aviation relations with the region’s countries and the direct overflight permission given to Israeli airlines flying to the east are expected to help develop air tourism and freight relations not only with regional markets but also with those in Southeast Asia.

TABLE 2

[1] Public opinion polls show that about 40 percent of the citizens of Saudi Arabia, the UAE, and Qatar favor relations with Israel, whereas only 10 percent of citizens of Jordan and Egypt do so, even though peace treaties between these countries and Israel were concluded decades ago. Source: Washington Institute for Near East Policy (January 19, 2023).

[2] This overview does not cover trade in business services—Israel’s main export industry—and investment relations with Middle East economies due to incomplete data.

[3] Agreements among the United States, Israel, and Egypt or Jordan that absolve goods produced in Israel, Egypt, and Jordan from American tariffs in order to promote cooperation among these markets. The agreement with Egypt continues to promote Israel–Egypt trade but the Israel–Jordan treaty has lost its importance due to the conclusion of a bilateral free-trade agreement between the United States and Jordan.

[4] Billions of Cubic Meters, the accepted unit of measurement for trade in natural gas.

[5] In January–September 2022, 39 percent of Emirati imports originated in eastern Asia and 18 percent in Europe, and almost half of them were re-exported to other Middle East countries. Source: Emirati Federal Competitiveness and Statistics Authority.

[6] Data: Federal Competitiveness and Statistics Authority. According to the Israel Central Bureau of Statistics, however, imports from the UAE of goods from other countries were only about one-fourth of Israeli imports from the Emirates. A misclassification of goods as products of the UAE may lead to future lenience in the importation of these goods under the Israel-UAE free-trade agreement. Re-exported goods from the Emirates to Israel originate in a wide variety of countries including Russia, China, Ukraine, and even Morocco and Brazil (CBS).

[7] We examine the effect of the expansion of imports from the UAE on import prices (including shipping and insurance) by comparing the specific prices (according to net weight in tons) of goods imported from the UAE (six-digit resolution in the HS code) with the corresponding prices of the same goods imported from India, China, and the rest of the world. The import prices were compared on the basis of data that the Israel Central Bureau of Statistics reported to Comtrade. The data pertain to January–September 2022 only. The weight of each good in the weighted average of import prices was determined on the basis of the share, in import value, of the same good to Israel in total goods imports to Israel in 2019 (on the eve of the COVID-19 crisis).

[8] Based on Ministry of Energy data, gas transmission infrastructure are expected to grow with the inauguration of a pipeline via Nitzana Crossing, projected to open in 2026, with a capacity of 3.5–6 BCM per year; expansion of capacity of the EMG pipeline to Egypt, planned for 2024, from 4.5 BCM to 7 BCM; and expansion of capacity of the gas pipeline to northern Jordan from 7 BCM to 10 BCM.

[9] Declaration of Intent between the Hashemite Kingdom of Jordan, the State of Israel, and the United Arab Emirates (November 22, 2022).

[10] Water sector overview at the U.S. International Trade Administration website (as of December 14, 2022).

[11] We have no official data on the number of Israeli tourists who visited Morocco, but one may estimate their number at more than 70,000 on the basis of the number of passengers on flights between these countries (Table 2) and the small number of Moroccan tourists visiting Israel.

[12] Incoming tourist arrivals in 2022 were 17,000 from Jordan, 8,000 from Egypt and Morocco combined, 1,400 from the UAE, and only 400 or so from Bahrain.

[13] A comparison of data on Israeli tourism to Turkey and the UAE with data on flights to these countries shows that about half of those flying to the UAE, and about one-third of those flying to Turkey, were Israelis on continuing flights or passengers without Israeli citizenship.