This document presents the forecast of macroeconomic developments compiled by the Bank of Israel Research Department in July 2017. The forecast was presented to the Monetary Committee on July 9, 2017, during its meeting prior to the decision on the Bank of Israel interest rate reached on July 10, 2017. According to the staff forecast, gross domestic product (GDP) is projected to increase by 3.4 percent in 2017 and by 3.3 percent in 2018. The rate of inflation over the next year (ending in the second quarter of 2018) is expected to be 0.8 percent. The Bank of Israel interest rate is expected to remain at its current level of 0.1 until the first quarter of 2018, and to increase gradually from the second quarter of 2018.

Forecast

The Bank of Israel Research Department compiles a staff forecast of macroeconomic developments on a quarterly basis. The staff forecast is based on several models, various data sources, and assessments based on economists' judgment. The Bank's DSGE (Dynamic Stochastic General Equilibrium) model developed in the Research Department—a structural model based on microeconomic foundations—plays a primary role in formulating the macroeconomic forecast.[1] The model provides a framework for analyzing the forces that have an effect on the economy, and allows information from various sources to be combined into a macroeconomic forecast of real and nominal variables, with an internally consistent "economic story".

a. The global environment

Our assessments of expected developments in the global economy are based mainly on projections by international institutions (the International Monetary Fund and the OECD) and by foreign investment houses. These institutions revised their forecasts for growth in advanced economies and for world trade slightly upward. Accordingly, our forecasts are for growth in advanced economies of about 2 percent in both 2017 and 2018. As for the world trade, we project growth of 4.6 percent in 2017 and 3.8 percent in 2018.

Based on assessments derived from the capital market (assessments based on interest rate futures contract prices), the US federal funds rate is expected to increase to 1.25 percent at the end of 2017 and 1.5 percent at the end of 2018. In contrast, the interest rate on deposits with the central bank in Europe is expected to increase very moderately from its current level of -0.4 percent, and to remain negative at -0.3 percent at the end of 2017 and -0.2 percent at the end of 2018.

The international financial institutions revised their forecasts of inflation in the advanced economies upward. Accordingly, our assessment is that inflation in the advanced economies will reach about 2 percent in 2017 and in 2018. The price of Brent crude oil declined during the second quarter, to about $47 per barrel.[2]

b. Real activity in Israel

GDP is expected to grow by 3.4 percent in 2017 and by 3.3 percent in 2018 (Table 1). The expected growth rate for 2017 was revised upward from the previous forecast, because National Accounts data for the first quarter and initial activity data for the second quarter show that exports and investments increased more than our assessment in the previous forecast. Our assessment is that in the forecast horizon (the next year-and-a-half), we will see a continued increase in the growth rate of exports, inter alia due to the expected recovery in world trade, and of investments in the various industries. In contrast, the growth rate of private consumption is expected to moderate after having been higher than the growth rate of the other uses and of GDP for a long time. Essentially, the forecast reflects a gradual transition to growth based less on private consumption and more on exports. It should be noted that the development of the real economic variables in recent quarters was influenced by vehicle purchases being brought forward due to changes in vehicle taxation that took effect in January 2017.[3] This is reflected, inter alia in the fact that the annual growth rate in 2017 is lower than it was in 2016, but our assessment is that net of this effect, it will be similar to the growth rate in 2016, and will be slightly higher than 3.5 percent. Further changes in vehicle taxation are expected in January 2019, and our assessment is that they will also lead to purchases being brought forward, which will increase the growth rate in 2018.[4]

|

Table 1 Economic Indicators |

|||

|

Research Department Staff Forecast for 2017 to 2018 |

|||

|

(rates of change, percent, unless stated otherwise; previous forecast in parentheses.) |

|||

|

|

Figures for |

Bank of Israel forecast |

Bank of Israel forecast |

|

|

2016 |

2017 |

2018 |

|

GDP |

4.0 |

3.4(2.8) |

3.3(3.3) |

|

Civilian imports (excluding diamonds, ships, and aircraft) |

8.1 |

2.5(2.0) |

8.0(8.0) |

|

Private consumption |

6.3 |

3.0(3.0) |

3.5(3.5) |

|

Fixed capital formation (excluding ships and aircraft) |

10.5 |

1.5(0.0) |

9.0(9.0) |

|

Public sector consumption (excluding defense imports) |

3.8 |

4.2(4.2) |

1.5(1.5) |

|

Exports (excluding diamonds and start-ups) |

1.5 |

5.0(3.5) |

4.0(4.0) |

|

Unemployment ratea |

4.1 |

3.9(3.6) |

3.9(3.6) |

|

Inflation rateb |

-0.3 |

0.5(0.8) |

1.5(1.5) |

|

Bank of Israel interest ratec |

0.10 |

0.10(0.10) |

0.50(0.50) |

|

a) Annual average of unemployment in the primary working ages (25–64). |

|||

|

b) Average CPI reading in the final quarter of the year compared with the final-quarter average in the previous year. |

|||

|

c) End of the year. |

|||

|

Source: Bank of Israel. |

|||

c. Inflation and interest rate estimates

In our assessment, the inflation rate in the four quarters ending in the second quarter of 2018 will be 0.8 percent and in 2018 it will be 1.5 percent. The prices of domestic products are expected to continue increasing moderately, as a result of moderating forces—including increased competition and government measures to lower the cost of living—that are expected to continue slowing the rate of price increases. In contrast, the fact that the labor market is near full employment is expected to continue supporting increased wages, which may lead to an increase in domestic inflation. The prices of imported products are expected to increase at a higher rate than that of the past two years, as inflation worldwide continues to increase. Expected inflation for the coming year is about 0.2 percentage points lower than the previous forecast for the equivalent period, mainly due to the expected effect of the decline in oil prices.

|

Table 2 |

|||

|

Inflation and interest rate forecasts for the coming year |

|||

|

(percent) |

|||

|

|

Bank of Israel Research Department |

Capital marketsa |

Private forecastersb |

|

Inflation ratec |

0.8 |

0.5 |

0.5 |

|

(range of forecasts) |

|

|

(-0.3–1.5) |

|

Interest rated |

0.25 |

0.16 |

0.18 |

|

(range of forecasts) |

|

|

(0.1–0.25) |

|

a) Daily average for the month of June. Seasonally adjusted inflation expectations. |

|||

|

b) Inflation and interest rate forecasts are those published after the publication of the CPI reading for May. |

|||

|

c) Inflation rate over the next year (Research Department: in the four quarters ending in the second quarter of 2018). |

|||

|

d) The interest rate in one year (Research Department: the interest rate in the second quarter of 2018). Capital markets forecast derived from Telbor rates. |

|||

|

Source: Bank of Israel. |

|||

According to the Research Department’s assessment, the Bank of Israel interest rate is expected to be 0.1 percent until the first quarter of 2018, and to start increasing in the second quarter of 2018. The interest rate is expected to remain at its current level in the coming year, in order to support the return of inflation to within the target range. The interest rate is expected to increase in the second quarter of the 2018, to 0.25 percent, following a number of quarters in which the inflation rate is expected to exceed 1 percent, and as one-year inflation expectations draw close to the center of the target range. The interest rate is expected to increase again in the fourth quarter of 2018 to 0.5 percent.

Table 2 indicates that the forecasts compiled by the Research Department regarding the interest rate and inflation in the coming year are slightly higher than the projections of private forecasters and expectations derived from the capital markets.

d. Balance of risks in the forecast

Several factors may lead to the domestic economy developing differently than in the baseline forecast. These include uncertainty concerning the future development of the exchange rate and the extent to which the appreciation of the shekel thus far will roll over to prices, as well as uncertainty concerning the extent to which government measures to reduce the cost of living will roll over to prices and regarding the possibility that the government may take further measures of this kind.

Regarding the global environment, even though the international institutions note that downward risks to growth and world trade have decreased, uncertainty remains regarding the pace of recovery of these variables. One of the main challenges facing policy-makers around the world is the creation of inclusive growth, the absence of which may lead to strengthening calls for pulling out of trade agreements and for implementing isolationist economic policies.

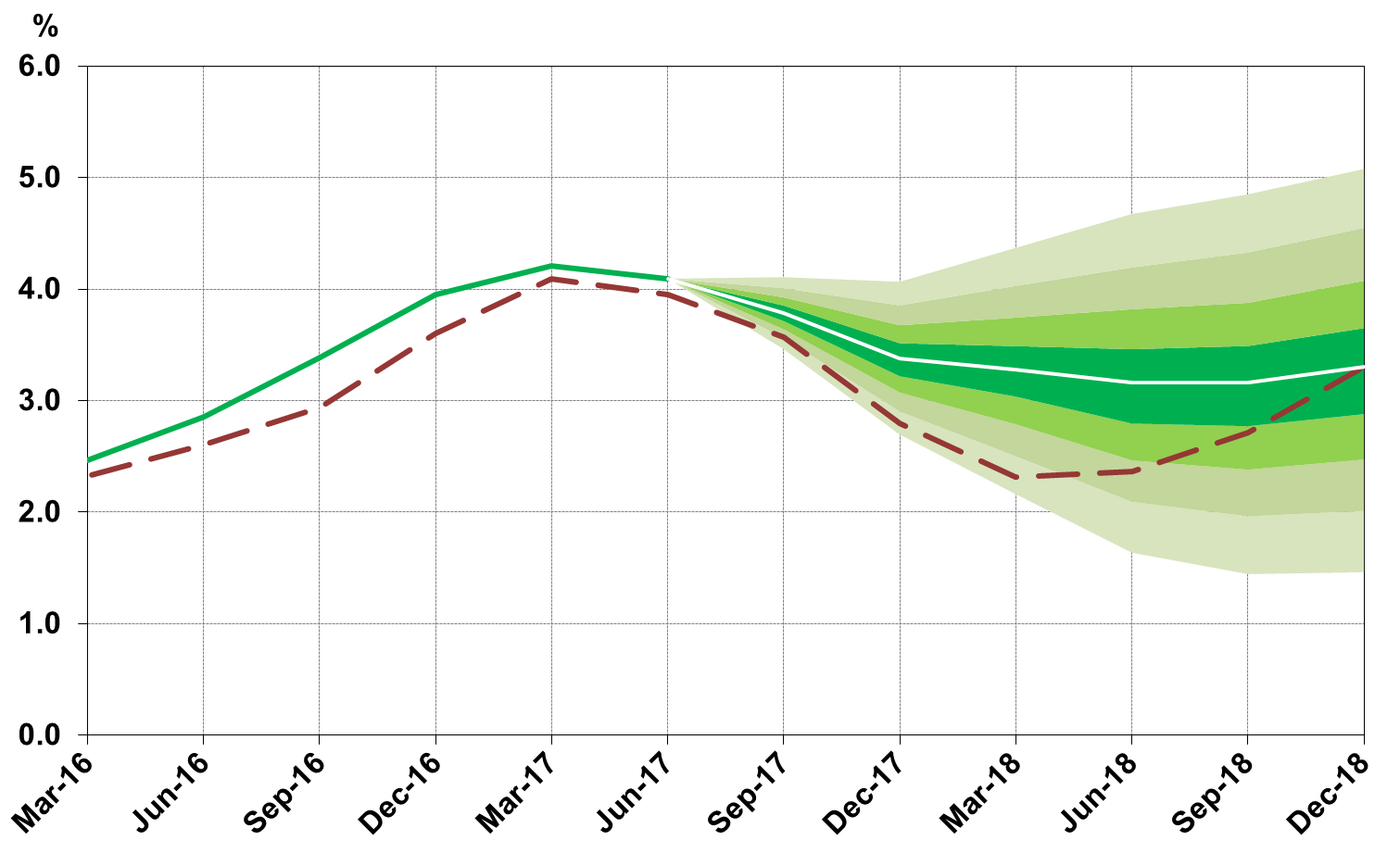

Figures 1 to 3 present fan charts around the inflation rate, interest rate and GDP growth forecasts. (The broken line represents the baseline forecast from April.) The width of the fan is derived from the estimated distributions of the shocks in the Research Department's DSGE model.

Figure 1

Actual Inflation and Fan Chart of Expected Inflation

(Cumulative increase in prices in the previous four quarters)

Figure 2

Actual Bank of Israel Interest Rate and Fan Chart of Expected Interest Rate

Figure 3

Actual GDP Growth Rate in the Past Four Quarters and Fan Chart of Expected Growth Rate

(Total GDP over the past four quarters relative to GDP in the preceding four quarters)

The center of the fan chart (the white line) is based on the Bank of Israel Research Department assessment. The width of the fan is based on the Department’s medium-scale DSGE (dynamic stochastic general equilibrium) model. The full fan covers 66 percent of the expected distribution. The dotted line corresponds to the previous staff forecast (published in April 2017). In terms of GDP growth (Figure 3), until March 2017, the dotted line reflects the data and estimates that were known at the time when the previous forecast was formulated, while the solid line reflects the updated data and estimates (the difference between them derives from new and data and revisions by the Central Bureau of Statistics to the data).

SOURCE: Bank of Israel Research Department.

[1] An explanation of the macroeconomic staff forecasts compiled by the Research Department, as well as a review of the models on which they are based, appear in Inflation Report number 31 (for the second quarter of 2010), Section 3c. A Discussion Paper on the DSGE model is available on the Bank of Israel website, under the title: “MOISE: A DSGE Model for the Israeli Economy,” Discussion Paper No. 2012.06.

[2] According to the average of the last two weeks of June.

[3] According to the National Accounts recording rules, taxation on imported vehicles is included in GDP. These imports also contribute to GDP through their effect on importers’ added value.

[4] Our estimate is that the growth rate net of this effect will be about 3.0% in 2018.