Abstract

This document presents the forecast of macroeconomic developments compiled by the Bank of Israel Research Department in June 2016. The forecast was presented to the Monetary Committee on June 26, 2016, during its meeting prior to the decision on the Bank of Israel interest rate for July 2016. According to the staff forecast, gross domestic product (GDP) is projected to increase by 2.4 percent in 2016 and by 2.9 percent in 2017. The rate of inflation over the next year (ending in the second quarter of 2017) is expected to be 1.0 percent. The Bank of Israel interest rate is expected to remain at its current level of 0.1 percent during the coming year, and to begin rising at the end of 2017.

Forecast

The Bank of Israel Research Department compiles a staff forecast of macroeconomic developments on a quarterly basis. The staff forecast is based on several models, various data sources, and assessments based on economists' judgment.[1] The Bank's medium scale DSGE (Dynamic Stochastic General Equilibrium) model developed in the Research Department—a structural model based on microeconomic foundations—plays a primary role in formulating the macroeconomic forecast.[2] The model provides a framework for analyzing the forces which have an effect on the economy, and allows the integration of information from various sources into a macroeconomic forecast for real and nominal variables, with an internally consistent "economic story".

a. The global environment

Our current assessments of expected developments in the global economy are based mainly on projections by international institutions (the International Monetary Fund and the OECD) and by foreign investment houses. Even prior to the referendum leading to the decision regarding the Brexit, these institutions revised their forecasts—for inflation, the interest rate, and growth in advanced economies—slightly downward. Following the referendum, a further downward revision took place with respect to the future interest rate path of the major central banks. Those are now not expected to rise before 2018, whereas the Fed and the bank of England are even expected to slightly reduce their interest rates in the near term. We assume that the GDP of the advanced economies will grow by 1.7 percent in each of the years 2016–2017. Based on scenarios analyzed by the IMF concerning possible effects of the Brexit before the referendum took place, we assume that the negative contribution of the Brexit to growth in 2017 is 0.2 percentage points. These are, obviously, preliminary assessments, before any decisions were made by Britain and the EU about the Brexit processes and, accordingly, before main details of these are revealed. Therefore, these assessments are subject to revisions. The forecast of goods and services imports to the advanced economies in 2016 is lowered as well, to growth of 3.1 percent in 2016 and by 3.7 percent in 2017, compared with growth of about 4.0 percent per year in the previous forecast from March.[3]

In contrast, we revised the expected price of oil upward following the marked increase since the publication of the previous forecast. The average price per barrel of oil (Brent crude) was about $47 during the second quarter (until late June), compared with an average price of about $35 per barrel during the first quarter.

b. Real activity in Israel

Table 1

Economic Indicators | |||

Research Department Staff Forecast for 2016 to 2017 | |||

(rates of change, percent, unless stated otherwise) | |||

Data for |

Bank of Israel forecast |

Bank of Israel forecast | |

2015 |

2016 |

2017 | |

GDP |

2.5 |

2.4 |

2.9 |

Civilian imports (excluding diamonds, ships, and aircraft) |

2.7 |

4.0 |

6.2 |

Private consumption |

4.9 |

4.3 |

2.8 |

Fixed capital formation (excluding ships and aircraft) |

-1.0 |

5.0 |

6.3 |

Public sector consumption (excluding defense imports) |

2.9 |

3.4 |

2.3 |

Exports (excluding diamonds and start-ups) |

-1.5 |

-1.5 |

4.4 |

Unemployment ratea |

5.2 |

5.2 |

5.2 |

Inflation rateb |

-0.9 |

0.0 |

1.2 |

Bank of Israel interest ratec |

0.10 |

0.10 |

0.25 |

a) Annual average. |

|||

b) Average CPI reading in the final quarter of the year compared with the final-quarter average in the previous year. | |||

c) End of the year. |

|||

Source: Bank of Israel. | |||

GDP is expected to grow by 2.4 percent in 2016 (Table 1). This rate of GDP growth is lower than the 2.8 percent of the previous forecast in March, mainly reflecting the low growth according to first quarter data, which was affected by the weakness of export data. The weakness of exports during the first quarter is exceptional, even compared to its development in recent years, but some of the factors that led to contraction in the first quarter seem temporary. Exports’ effect on growth was slightly offset by solid growth in domestic uses, which were supported inter alia by employment data and the interest rate. During the second half of 2016, the assessment is that private consumption will remain robust, although its rate of growth will moderate slightly, that fixed capital formation (both investment in construction and investment in the primary industries) will show solid growth, and that exports will transition from contraction to growth.

The growth forecast for 2017 was reduced slightly, to 2.9 percent (compared with 3.0 percent in the previous forecast, and before the Brexit). While growth is expected to continue to rely on the robustness of domestic demand, our assessment is that it will also be influenced by the exhaustion of the increase in the supply of labor that has characterized recent years, and by some weakness in some of the export industries.

Investment in 2017 is expected to increase by 6.3 percent, both due to investment by a large company (which will be attributed almost completely to the import of machines and equipment), and due to the expected increase in investment in construction later in the year. Exports are expected to return to growth in 2017 (by 4.4 percent), inter alia as a result of increased exports of electronic components due to the investment mentioned above. Due to the high level of private consumption and the increase in its share of GDP and of uses following a long period of rapid growth, our assessment is that in 2017, the growth rate of private consumption will moderate slightly, to 2.8 percent, similar to the GDP growth rate. The growth of imports is expected to accelerate to 6.2 percent in 2017, to a large extent as a result of the investment mentioned above.

As of now, the government has still not decided on the framework and structure of the 2017 budget. The forecast assumes a real increase of 2.3 percent in public consumption in 2017 (compared with an increase of 1.4 percent according to the previous forecast).

c. Inflation and interest rate estimates

In our assessment, inflation in the four quarters ending in the second quarter of 2017 is expected to be 1.0 percent. We assess that inflation in the coming period will be affected by a labor market that is near full employment, which is even characterized by supply constraints in some industries, but that it will also be affected by increased competition.

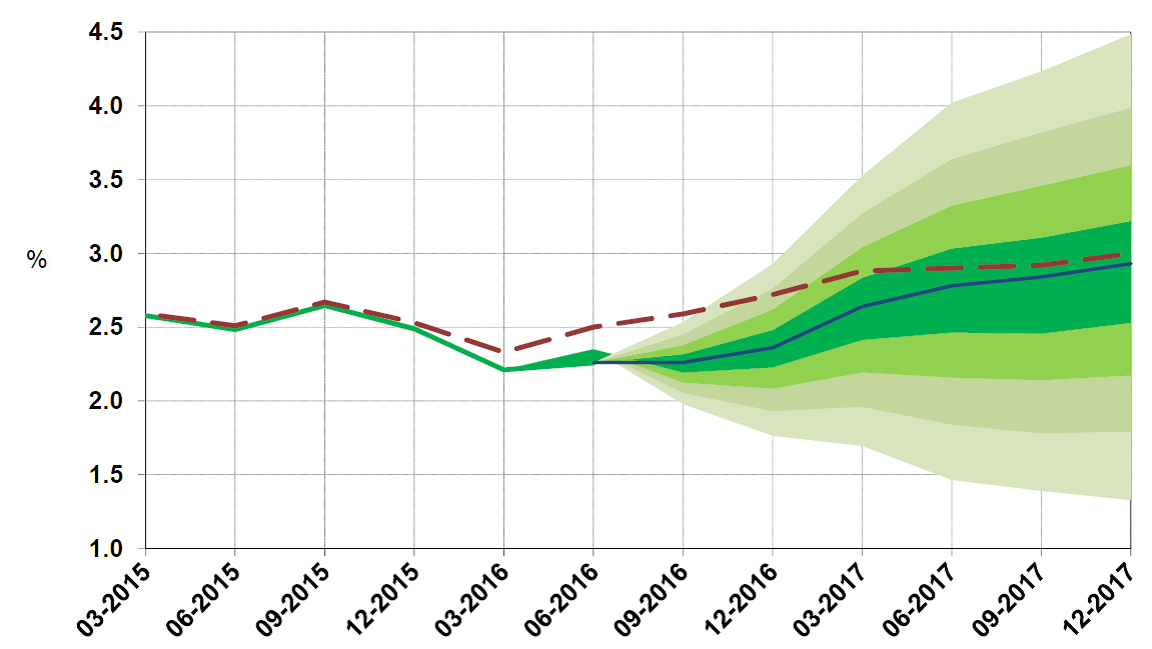

According to the Research Department’s assessment, the Bank of Israel interest rate is expected to be 0.1 percent until the third quarter of 2017, and to start increasing thereafter. This path reflects a balance between the need to bring inflation to its target and to support real activity, and the need to maintain financial stability. This path of the interest rate also takes into account the expected paths of interest rates in the US and in other economies—which, as mentioned above, were revised downward since the previous forecast, and in particular since the Brexit vote. Figure 2 shows that the expected path of the interest rate in 2017 is lower than what was published in the previous forecast.

Table 2 compares the Research Department’s forecasts with expectations derived from the capital markets and projections of professional forecasters. The table indicates that the forecast compiled by the Research Department regarding the interest rate in the coming year is similar to expectations derived from the capital market and to the projections of professional forecasters.[4] With that, the forecast compiled by the Research Department regarding inflation in the next year is higher than that of the professional forecasters, on average, and is higher than expectations derived from the capital market.

Table 2 | |||

Forecasts for inflation rate and interest rate for the coming year | |||

(percent) | |||

Bank of Israel Research Department |

Capital marketsa |

Private forecastersb | |

Inflation ratec |

1.0 |

0.4 |

0.8 |

(range of forecasts) |

(0.1–1.1) | ||

Interest rated |

0.1 |

0.1 |

0.10 |

(range of forecasts) |

(0.0–0.5) | ||

a) Daily average for the month of June (up to June 22). Seasonally adjusted inflation expectations. | |||

b) Inflation and interest rate forecasts are those published after the publication of the CPI reading for May. | |||

c) Inflation rate over the next year (Research Department: in the next four quarters). | |||

d) The interest rate in 1 year (Research Department: the interest rate in the second quarter of 2017). Capital markets forecast derived from Telbor rates. | |||

Source: Bank of Israel. | |||

d. Balance of risks in the forecast

This forecast is contingent on assumptions related to the global environment and to domestic background conditions. Developments different from those assumptions may lead to developments in the domestic economy that are different from those in the forecast. There is a high degree of uncertainty with regard to the actual measures that will be taken by the UK and the EU as part of the Brexit, let alone their expected implications. The actual ramifications may be inherently different than those assumed in this forecast. But even before accounting for the Brexit, the advanced economies are internalizing the low growth rates of recent years, compared to the higher growth rates of the past. Therefore, global assessments are for a reduced likelihood of an increase in the growth rate to past levels. In addition, the low levels of short-term interest rates make it difficult to adopt more accommodative monetary measures, if necessary. The volatility of oil prices is also a source of uncertainty that impacts the risks to the forecast.

Domestic risk factors include the uncertainty regarding developments of the exchange rate, and in relation to fiscal policy for 2017.

Figures 1 to 3 present fan charts around the inflation rate, interest rate and GDP growth forecasts. (The broken line represents the baseline forecast from March.) The width of the fan is derived from the estimated distributions of the shocks in the Research Department's DSGE model.

Figure 1

Actual Inflation and Fan Chart of Expected Inflation

Actual Inflation and Fan Chart of Expected Inflation

(cumulative increase in prices in previous four quarters)

Figure 2

Actual Bank of Israel Interest Rate and Fan Chart of Expected Interest Rate

Actual Bank of Israel Interest Rate and Fan Chart of Expected Interest Rate

Figure 3

Actual GDP Growth Rate in the Past Four Quarters and Fan Chart of Expected Growth Rate

(total GDP over the past four quarters relative to GDP in the preceding four quarters)

The center of the fan chart is based on the Bank of Israel Research Department assessment. The width of the fan is based on the Department’s medium-scale DSGE (dynamic stochastic general equilibrium) model. The full fan covers 66 percent of the expected distribution. The dotted line corresponds to the pervious staff forecast (published in March 2016).

SOURCE: Bank of Israel.

[1] An explanation of the staff macroeconomic forecast, and an overview of the models on which it is based, can be found in Inflation Report 31 for the second quarter of 2010, section 3-C.

[2] A Discussion Paper on the model is available on the Bank of Israel website, under the title: “MOISE: A DSGE Model for the Israeli Economy,” Discussion Paper No. 2012.06.

[3] We assume that the Brexit will reduce imports to the advanced economies by 0.3 percent in 2017, and, as a result, reduce Israeli exports by 0.3 percent.

[4] The forecasts of private forecasters and the market-based expectations refer to the period prior to the Brexit referendum.